High-yield investors bracing for a downturn in 2018 can relax. By some metrics, high-yield companies have rarely looked better. The way we see it, investors who do their homework can still profit in this environment.

After a strong 2017, high-yield bonds have struggled this year as US Treasury yields spiked and inflation potential stirred up fears that the Federal Reserve may raise borrowing costs more aggressively. With the US credit cycle in its 10th year and credit spreads—the extra yield high-yield bonds offer over comparable government debt—near record lows, some investors are no doubt asking themselves whether high yield’s potential return is worth the risk.

The answer, as far as we’re concerned, is yes. What makes us so sure? Simply this: in high yield, there are three warning signs that usually precede trouble—and none of them are flashing red yet. Let’s take a closer look.

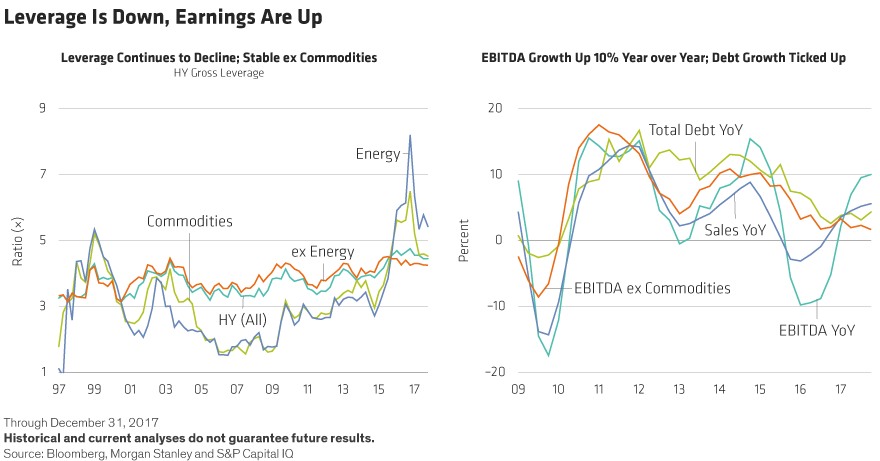

Warning Sign No. 1: When Leverage Ratios Are High and Rising

Financial leverage is a lot like the water in a major river: when it’s high and rising, we start to worry—especially if we’re late in the credit cycle. But over the past few years, leverage has been declining in the high-yield market, leaving it less vulnerable to today’s rising-rate and late-cycle environment.

Energy companies are one reason for this. Many went on a borrowing binge earlier in the decade when commodity prices were high. Since the collapse of prices in 2014 and 2015, leverage in the sector has come down sharply. But leverage has been remarkably stable in the rest of the market too. This is partly because strong corporate earnings have vastly increased cash flow. But even after a 10% increase in EBITDA growth in 2017, companies simply haven’t been stretching to make large capital expenditures or buy back stocks (Display 1).

In the US, many companies may be concluding that now isn’t the time to ramp up leverage. Yes, solid economic growth has been a boon for many issuers. And comprehensive US tax reform is likely to boost earnings this year. But after that, most companies expect the rate of earnings growth to slow and appear to be acting responsibly.

In Europe, leverage ratios are down, too, largely the result of stronger eurozone growth and improving corporate fundamentals.

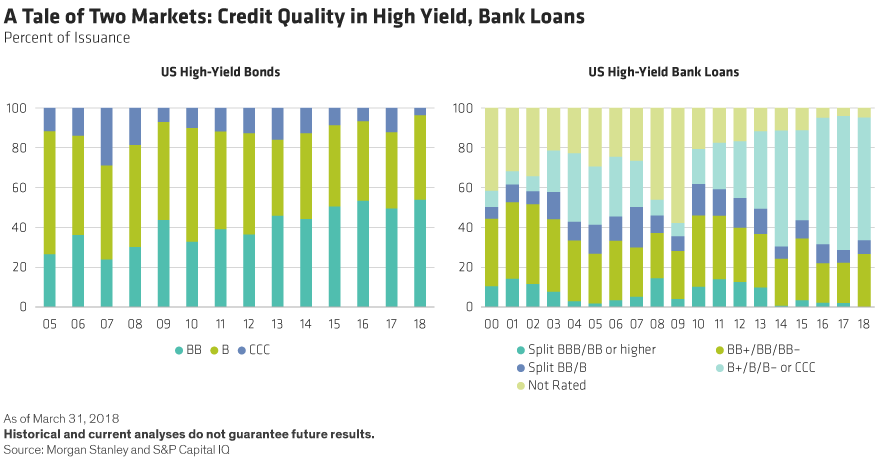

Warning Sign No. 2: When “Junk” Issuance Dominates

CCC-rated “junk” bonds—the riskiest part of the high-yield market and the most vulnerable to rising rates—accounted for about 12% of new issuance in 2017—and just 3.5% in the first quarter of 2018. Compare that to 2007, when 28% of the high-yield bonds issued were rated CCC.

This is important, because when CCC-rated bonds dominate, it’s a sign that investors are hunting for yield and ignoring credit quality. This makes it possible for companies with fragile finances to borrow at attractive rates and leaves the market more vulnerable to a sharp drawdown.

What’s keeping a lid on CCCs? The volume of mergers and acquisitions (M&A) has been falling. More importantly, leveraged buyouts (LBOs)—the riskiest sort of takeover, which involves adding significant debt to corporate balance sheets—have been getting even rarer; last year, they accounted for 17% of debt issuance, compared with 29% in 2008. In the first quarter of 2018, just 1% of high-yield issuance came from LBOs (Display 2).

As Display 2 also illustrates, we’ve seen the opposite trend in the high-yield bank-loan market. There, M&A and LBO activity is on the rise—largely because investors who see floating-rate loans as a remedy for rising rates are buying first and asking credit questions later. This is allowing companies to borrow without offering the types of lender protections typical in the high-yield market. It also makes loans less effective against rising rates.

Warning Sign No. 3: A Wave of High-Yield Defaults

Put simply, we’re not seeing anything that resembles a surge in defaults. Default volume ticked higher in the first quarter to 2.21%, with a single issuer (iHeartCommunications) accounting for more than half of the total.

Despite worries about inflation, the Fed is still signaling that it will hike rates gradually, and the global economy remains strong. If you’re betting that growth will continue this year and inflation will stay under control, you shouldn’t expect a wave of defaults any time soon. We expect a slight year-over-year rise, but for the rate to remain below average.

Today’s low default rates suggest high-yield bonds may not be as expensive as they first appear. As of mid-May, the yield to worst for the broad market—the lowest likely return you should get barring significant defaults—was hovering around 6.3%. For the global market, it was 6.1%. Few other assets can provide that type of income potential; those that can usually come with higher risk.

Don’t Ditch; Diversify.

None of this means that there won’t be rough patches ahead for high-yield bonds and other risk assets. With central banks slowly shifting out of the quantitative-easing era, markets are likely to remain volatile.

Our advice for surviving and continuing to profit in these conditions: Use a global, multi-sector strategy that mixes high-yield bonds with other income generators, such as emerging-market bonds and US securitized assets. And be selective. No matter the sector, a set-it-and-forget-it approach isn’t the way to go. But shunning high-yield bonds—one of the highest potential income generators out there—isn’t an option either.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.