Speculation is building about a looming shake-up in the leadership of the US Federal Reserve. Transitions are nothing new—but the stakes this time are unusually high for the economy and markets.

The biggest question on investors minds: Who’ll lead the Fed? Janet Yellen’s four-year term as chair of the Board of Governors expires February 3, 2018, though her term as a Board governor runs until 2024. Yellen could stay on the Board even if President Trump doesn’t reappoint her, but it’s almost certain that she’d resign.

Based on past experience, we expect the president to announce a nominee for Fed chair in the next couple of months. Which names are being talked about right now?

The most commonly mentioned candidates include Yellen, as President Trump could simply choose to reappoint the Fed’s leader. Current Fed governor Jerome Powell, another candidate, would provide a measure of continuity. John Taylor’s name has been floated, too. A Stanford professor, Taylor is a well-respected thinker on monetary policy issues—and he’s also more likely to make dramatic changes.

Also on the list: Gary Cohn, director of the National Economic Council and former second-in-command at Goldman Sachs. Then there’s Kevin Warsh, a former Board member who has become a vocal critic of the Fed’s efforts to support growth. No one knows who the eventual choice will be—and a dark-horse candidate could certainly emerge.

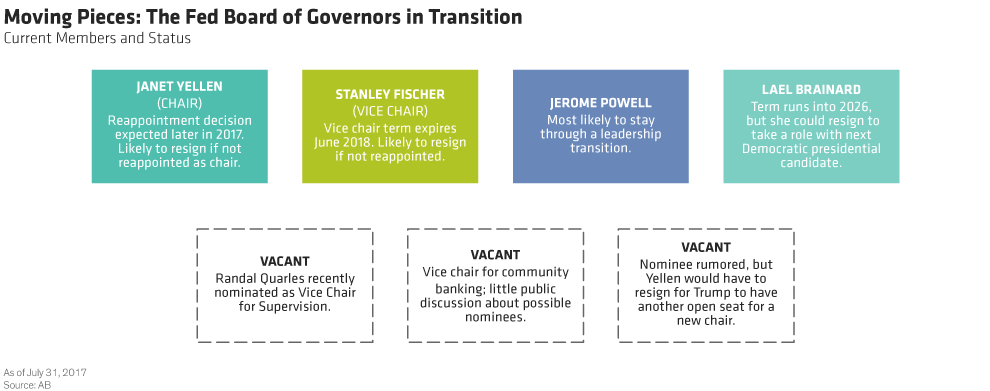

Winds of Change Throughout the Fed System

Change isn’t happening only at the top. Three seats on the seven-member Board of Governors are currently open (Display). If the president doesn’t reappoint Yellen as chair but does fill the current and potential vacancies, it seems likely that the Board will have six members with less than a year’s experience by the end of 2018.

The Fed’s regional District banks have seen leadership changes, too—and some bank presidents serve alongside the Fed Board members on the Federal Open Market Committee (FOMC). These comings and goings further reduce the experience level on the FOMC, and if the incoming Fed chair is a newcomer, the job will be that much harder.

Stakes Are High for Policy and the Markets

Of course, broad turnover isn’t unusual at the Fed, but there’s a lot at stake this time around. The Fed has become critical to financial markets over the past decade—from QE 1 through the taper tantrum and now the transition to interest-rate hikes and toward balance-sheet normalization. A changing of the guard brings different perspectives and policy philosophies, and the ultimate mix is hard to forecast.

We think the looming turnover at the Fed is one reason why the FOMC seems eager to start reducing its balance sheet. That way, the current committee could hand the new team a process that’s already in place and (ideally) running smoothly. There would be less need for the new leaders to make big decisions as soon as they’re in their seats.

Of course, the current FOMC wouldn’t shrink the balance sheet just to create a smoother transition, but the changeover does give it more incentive to make the move now. In fact, this consideration is, in part, why we feel strongly that balance-sheet reduction will start by the end of the summer in the US.

Decisions, Decisions, Decisions…

Balance-sheet reduction is part of a broader path of policy normalization that will put a lot on the Fed’s plate during this period of change.

Key decisions ahead include managing the relationship between reducing the balance sheet and the pace of interest-rate hikes. Financial-sector regulation is also on the agenda: it will take a lot of political skill to navigate the Trump administration’s priorities and the existing regulatory infrastructure—both domestically and internationally.

Then there’s the matter of communication. Financial markets tend to hang on the Fed’s every word. With so many new players, will the institution’s style and approach to communicating change?

In short, the identity of the new Fed chair—or Yellen, if she’s renominated—and the makeup of the Board of Governors will matter a lot to markets. Investors have come to rely on stability and predictability from the Fed. If that changes—or if investors think it has changed—capital markets could be more volatile in 2018 and beyond.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.