October’s 20th National Congress of the Communist Party of China (NCCPC) will be historically significant, but it’s not the only policy-making body that investors should be watching. The key to spotting clues about policy change in China lies in understanding the broad government structure.

The NCCPC, which takes place every five years, is the highest-profile event in China’s political calendar, providing a forum for leadership and constitutional changes. This year’s event will have particular symbolic significance, being the first since the Party’s centenary in 2021.

It’s also likely to be one of the most unusual and important in the Party’s history, as it will confirm President Xi Jinping as leader for an unprecedented third term and underline the importance of his thinking, much of which has already been incorporated into the constitution.

But investors seeking signs of policy changes—such as an end to the zero-COVID policy, or an easing of regulations and further cyclical stimulus—are likely to be disappointed. That’s because the NCCPC is an important guide to long-term structural policy, rather than short-term cyclical policy.

For clues about short-term policy, investors should look to other bodies that sit within China’s policy framework. To do this, it helps to have an overview of how China’s government works.

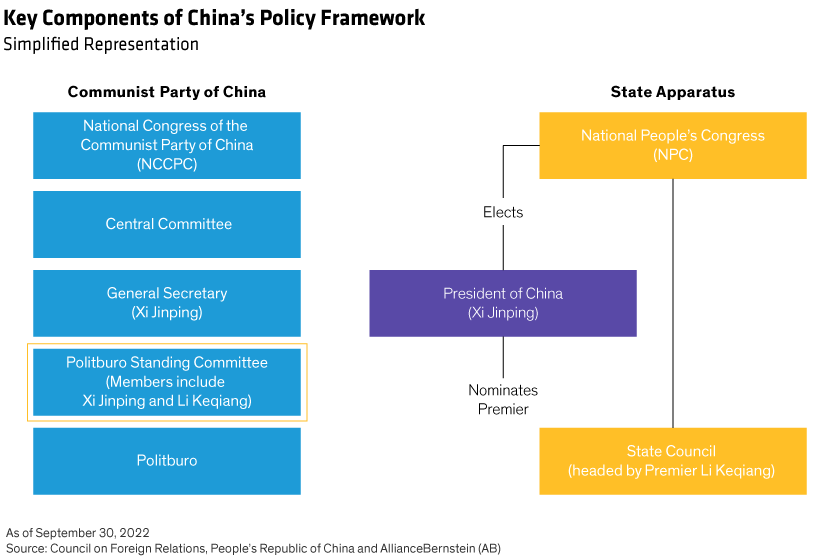

Party and State: Key Components

The basic power division in China is between the Party and the state apparatus. In the Party hierarchy, the most important bodies are the NCCPC and the Central Committee. The NCCPC elects the Central Committee, while the general secretary, politburo and Politburo Standing

Committee are elected at the first plenum1 of the Central Committee held after the NCCPC (Display).

The highest-ranking body in the state apparatus is the National People’s Congress (NPC), which meets annually, typically in March. The NPC elects the president—a role which, since 1993, has been held by the Party’s general secretary. The president in turn nominates the premier or head of government (ratified by the NPC), who presides over the State Council.

The country’s two most powerful executive officers—General Secretary of the Party Xi Jinping and Premier Li Keqiang—serve on the seven-member Politburo Standing Committee. As we discuss below, the Politburo Standing Committee and State Council, along with the NCCPC, are the key policy bodies for investors to watch.

What to Expect From the NCCPC

Three outcomes are likely from the upcoming NCCPC, in our view: further consolidation of President Xi’s power, a number of personnel changes at senior levels of government, and broad confirmation of structural policy settings.

One reason this year’s NCCPC is different from its predecessors is that it follows the introduction in 2021 of the “two establishes” idea, which establishes Xi as the core of the Party and its Central Committee, and the guiding role of what is officially known as Xi Jinping Thought on Socialism with Chinese Characteristics for the New Era.

Xi’s thoughts on economics—such as his view that China faces a deteriorating external situation (particularly in its relations with the United States)—also set the scene, together with the downward trend in economic growth and attempts to transition to a more consumption-driven growth model.

The most interesting personnel changes will be those affecting members of the Politburo Standing Committee, particularly Premier Li Keqiang, who is nearing the two-term limit of his time in office. He is not quite at retirement age so, in theory, could step down as premier into another role.

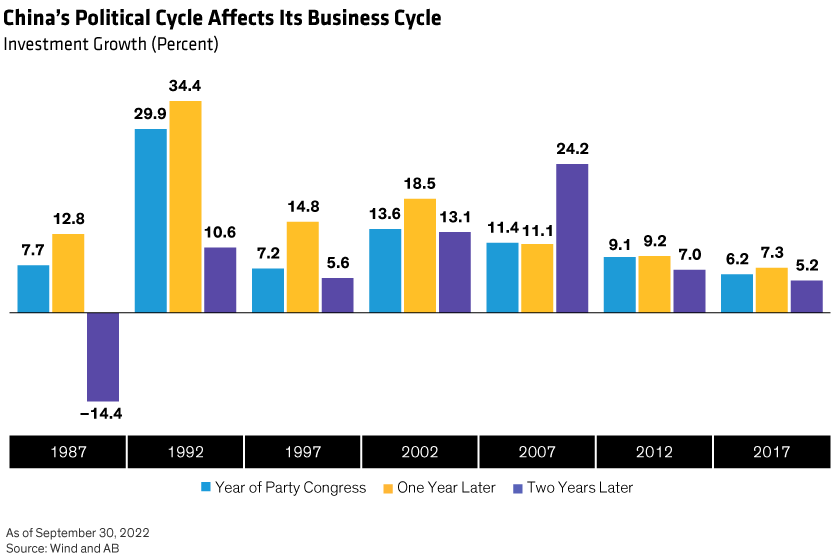

Investors should note, however, that personnel changes, in aggregate, may have positive implications. Investment growth has often ticked upward after an NCCPC as newly promoted local officials, keen to shore up their career credentials, encourage economic activity (Display).

Given that the country’s economic challenges are likely to persist for some time, however, any uptick following this year’s NCCPC is likely to be milder than in the past.

We expect few, if any, signals for changes to long-term structural policy. Pronouncements in this area are likely to be in line with the major elements of Xi’s thoughts in the 14th Five-Year Plan. Released in early 2021, it includes long-term objectives through 2035.

Investors, however, should also keep an eye on the plenums that follow the NCCPC, as these could provide clues about long-term policy changes. The third plenum typically discusses important high-level policy and reform topics while the fifth plenum addresses the Five-Year Plan.

Will the NCCPC End the Zero-COVID Policy?

The NCCPC, in our view, is unlikely to result in an end to the zero-COVID policy, although there may be further moderation of the rigor with which it is applied. In fact, we see no end to the policy until more older adults have been vaccinated. So far, about 67% of those older than 60 have received their third shots, but only 38% of those over 80.

But the daily vaccination rate has been low recently, at around 30,000. According to Goldman Sachs estimates, providing 80% of the population over 60 with a booster shot by year-end would require a daily vaccination rate of about 300,000—a great challenge in such a short period.

Clearly, the immunization of a significant share of the older population is a prerequisite to any policy easing. But the prospects for a short-term resolution seem even more unlikely, given the political considerations that policymakers have attached to it.

At a recent politburo meeting, President Xi said the issue should be viewed as long-term and systematic and, from a political perspective, in terms of the relationship between pandemic control and economic development. There is, then, no certainty as to when or how the zero-COVID policy will end.

For short-term cyclical policy clues, the politburo and State Council are better places to look.

China’s Short-Term Policy Channels

The major forums to set cyclical policy direction are the politburo meetings in April, July and December. After the December meeting, the Central Economic Work Conference, hosted by President Xi and consisting of senior national and local officials, elaborates policy for the year ahead.

Its messaging is reflected in the premier’s working report—which can include specific numerical economic targets, such as GDP growth targets and the budget deficit—to the NPC in March.

Weekly State Council meetings hosted by the premier are also important for cyclical policy and may provide the occasion for significant policy announcements.

Investors, in other words, should be looking at more than the NCCPC for policy clues.

NCCPC Is One Piece of the Puzzle

Indeed, the secret to understanding China’s evolving policy environment, in our view, lies in continuously monitoring its various facets, paying close attention to key government documents and speeches and articles by the country’s senior leaders.

The official journal Qiushi has recently republished speeches given by President Xi during the last two years. Those who have been paying less attention may mistake these republished articles for announcements of new policies, while these policies have, in fact, been in place for some time.

For astute China-watchers, however, they serve as a reminder of the NCCPC’s role as a forum to affirm the importance of Xi’s thinking.

1Seven plenums are usually held during the five years between each NCCPC.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.