Commodities haven’t been kind to investors in recent years. But we believe that shifting the frame of reference away from underlying price trends of metals and raw materials can reveal surprising opportunities in select commodity stocks.

The MSCI ACWI Commodity Producers Index has declined by 28% from the beginning of 2013 to the end of July 2015. Nonenergy commodities have fared even worse—the MSCI World Metals and Mining Index has dropped nearly 50% over the same period. Prices have plummeted because of concerns about slowing Chinese demand, coupled with continued supply growth in many key commodities such as iron ore and coal.

Looking Beyond Commodity Prices

These supply and demand conditions are likely to persist for some time, in our view. Yet we believe that there are still investment opportunities to be found. The trick is to identify commodity-related companies that don’t rely on rising prices of the underlying commodity to grow their earnings.

So what should you look for? Target companies or industries in which:

•Strategy or business models are shifting

•Spending and capital expenditure cuts are driving improved cash flow and margins

•Incremental cash flows are being used to boost dividends or reduce debt

Russian Steel: Back from the Brink

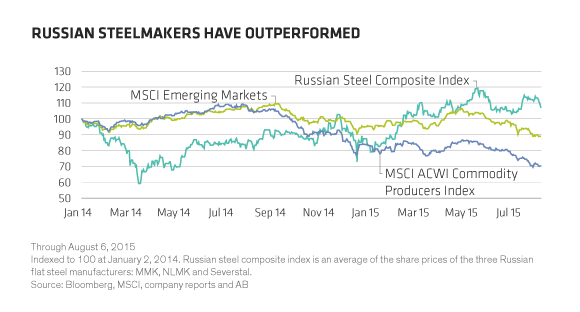

Take the Russian steel industry as an example. Despite declining global steel prices, stocks of Russian steelmakers have strongly outperformed the MSCI Emerging Markets, and Commodity Producers indices from March 2014 through today (Display). They’ve also outperformed the broader Russian index. So how did the industry pull it off?

It started with a structural advantage. Russian steel companies generally have large-scale facilities, low labor costs and backward integration into low-cost raw materials. Together, these factors ensured Russia was the cheapest producer of steel in the world over many years.

Many Russian steel companies enjoyed excess profits during the boom years of 2004–2007. But this also fueled hubris among controlling shareholders, who yearned to become dominant global players. To fulfill this dream, Russian companies started buying poor-quality assets abroad, believing they could improve them.

About three years ago, it all fell apart. By 2012, Russian steelmakers were burdened with massive debts, and their overseas operations were losing money as global steel markets deteriorated. To make matters worse, the Ukrainian crisis triggered sanctions against Russia, which threatened domestic economic growth, steel demand and access to debt markets.

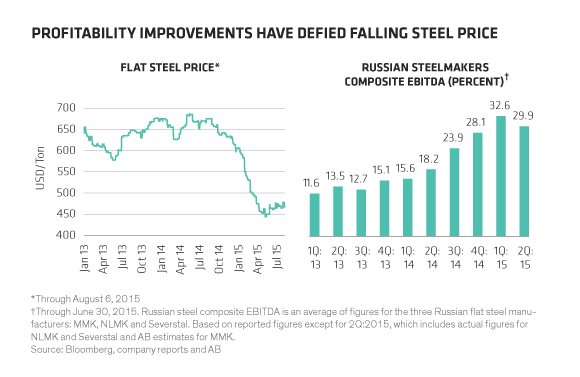

Investors who lost faith in the sector may have pulled the plug too quickly. First, the performance of Russian assets held up much better than the market expected. In fact, these companies benefited from the ruble’s collapse, which drove Russia’s low-cost position even lower. Despite sharp declines in Russian steel demand, operations continued at full capacity, driven by exports to Europe and the Middle East, which displaced local high-cost production. And since global steel prices are denominated in US dollars—even in Russia—profit margins for the Russian steel players actually expanded (Display).

Second, the controlling shareholders realized the errors of their ways. Many sold or spun off unprofitable foreign units and curtailed investment in new capacity in Russia. Debt was paid off and dividend payouts were increased. By mid-2014, a reduction in capital expenditures and asset sales drove enhanced free-cash-flow generation.

From Paper to Gold

Similar cases can be found across the commodity sector. Examples include Sappi, a paper producer, which faced a sharp drop in demand because of increasing electronic communications, and transformed its business to focus on more profitable specialty pulp used in textile manufacturing. In Turkey, gold-mining company Koza Altın has outperformed peers by becoming a trendsetter with innovative production and processing methods that are now being emulated throughout the industry.

Investors should take note of these stories. Instead of steering clear of commodities, we believe the downturn across the sector is a perfect time to hunt for industries and companies that can withstand the pressure. By staying active, investors can develop high conviction in unloved pockets of the commodities market that offer powerful countercyclical return potential for contrarian positions.

This blog was originally published in InstitutionalInvestor.com.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.