Bond investors are clearly worried about rising rates in today’s environment. Many are protecting themselves by moving to very short-term investments, or even cash. But is their “safe” choice putting them at risk?

The View Gets Better Up High

We get it. It seems intuitive that if interest rates are rising, bond prices will fall, so you should put your money someplace else. At least for now. The problem is, what’s intuitive isn’t always correct. In fact, investors who put their money into cash or similar strategies at this point in the rate cycle will find themselves quickly underperforming those who stuck to their bond strategy.

That’s not finger crossing. We can say that with a high degree of accuracy. That’s because—the rare default aside—bonds are predictable! They’re predictable because they have cash flows. And the higher the income, the larger the cash flow.

Where to Position the Most Important Statistic in Your Bond Portfolio

Bond returns come from two places: changes in price and coupon income. When interest rates rise, prices fall, which causes a short-term loss.

But in the long run, rising rates are good for bond investors, and here’s why: the income they generate in the form of coupon payments gets reinvested at new and higher rates.

What’s more, as the overall income level (average yield) rises, the buffer against price loss increases too. For example, a year ago, the 10-year US Treasury yielded a slim 2.21%, making it more vulnerable to an initial negative return. On June 1, 2018, it yielded 2.89%, a full 0.68% higher. All else being equal, a given interest-rate increase will have less of an effect on its total return today.

Also, it’s worth keeping in mind that a bond’s price tends to drift back toward par as it moves closer to maturity. This, too, can cushion the impact of escalating rates and falling prices.

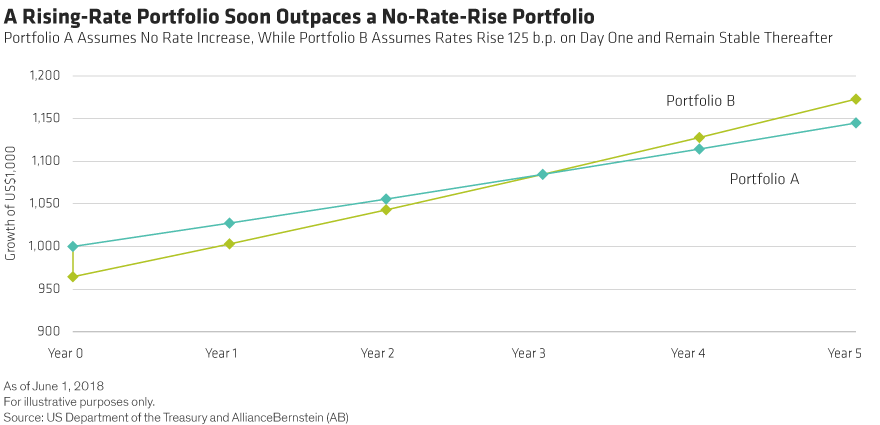

But let’s walk through an example to show what the actual impact of rising rates might be on a bond portfolio. We’ve modeled a simple portfolio of Treasury bonds and “shocked” it by assuming a sudden 125-basis-point rise in rates. What would its immediate performance look like? And then, how would the following years unfold (Display)?

At first, the portfolio sees an initial price loss—an undeniably painful experience. Even so, the portfolio still generates income, and investors who stay the course can reinvest that income at a higher yield. This helps to make up for the price loss and eventually offsets it altogether; before a year is out, our portfolio is back in the black. And by year three, the portfolio has not only caught up to where it would have been had rates never risen, but thereafter it’s worth more and is growing faster. After this point, you’ll be better off having stayed invested.

Here’s our rule of thumb: as long as the duration of your portfolio is shorter than the investment horizon, rising rates will benefit you—no matter how large the rate increase.

How Far Along Is This Cycle?

Since January 1, the 10-year US Treasury yield is up 43 basis points. It breached the 3% mark in mid-May—a threshold from which it has since retreated, but which it is likely to pass again. The two-year Treasury yield is up 55 basis points since the start of the year.

Strong economic growth and, to a lesser degree, increased inflation pressures are driving rates up. But—critically—the path is slow, well-signaled and steady, not sudden, surprising and shocking. We expect yields to continue to trend slowly higher for the next few months. As for the Fed, we expect three to four more rate hikes in 2018 before the central bank pauses to assess.

Did someone just mention inflation? It’s slowly climbing, and taking refuge in cash and very short-term investments is a surefire way to lose out to it. And fiscal indiscipline could create even more problems in the future by pushing rates up even faster.

Shifting to cash could soon have you lagging both income-generating bonds and inflation. And don’t expect to time the end of the interest-rate cycle, either. Not even the most seasoned bond managers can do that.

Let Time Help Buoy Your Returns

Rising interest rates aren’t the disaster the headlines would have us fear. Instead, they work to investors’ advantage. As with most things in life, the challenge is simply to keep calm, and carry on.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.