A pending US interest-rate hike and worries about inflation may have persuaded investors to start avoiding bonds. We think that’s a mistake, especially when it comes to high yield, a sector that often thrives when rates rise.

Bonds, of course, are highly sensitive to interest-rate movements—when rates rise, prices fall. And rising rates can certainly create short-term volatility. We’ve seen our share of it in the past few weeks.

The volatility—and the anxiety bond investors are feeling—increased after Donald Trump won the US presidential election and markets began betting his policies would trigger a jump in inflation. This scenario could convince the Federal Reserve to follow an interest-rate hike in December with several more in 2017.

But remember, interest rates have been low for decades and inflation in developed economies all but evaporated in the years after the global financial crisis. Investors have grown accustomed to this situation. The reaction to tighter Fed policy and possible reflation in financial markets, including high yield and other credit markets, isn’t a big surprise.

The good news is that the backup we’ve seen in bond yields is largely self-correcting; higher yields eventually lead to higher returns. That’s because as bonds mature, their prices drift back toward par. Investors who sit tight will soon be able to reinvest the principal from maturing, called or tendered securities and the coupon income that their portfolios pay in newer—and higher-yielding—bonds.

LOOKING PAST VOLATILITY

It’s also important to remember that in high yield sell-offs tend to be short-lived. Over the past two decades, high yield has recovered most big drawdowns—losses of more than 5%—in less than a year.

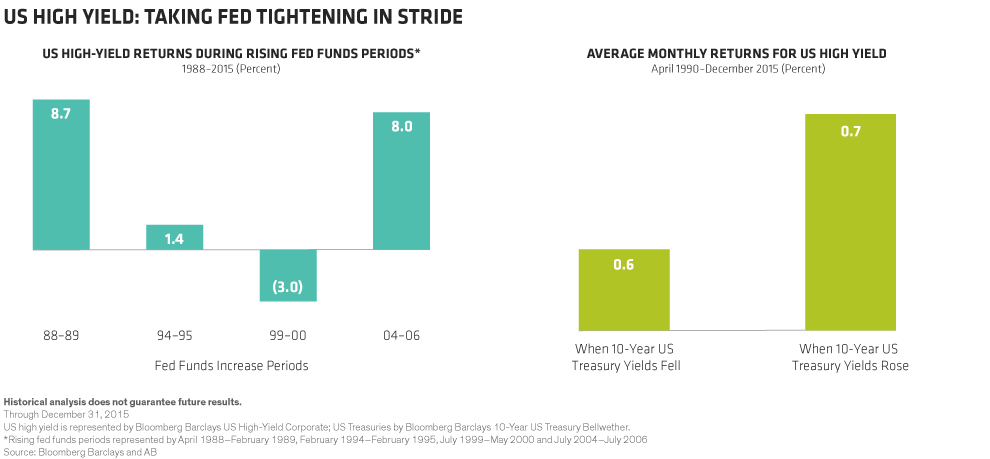

US high-yield bonds also have a strong track record during periods of Fed tightening (Display). This is partly because high yield isn’t closely correlated with interest rates. Rather, the bonds are strongly linked to the business results and fundamentals of the companies they represent. When the Fed raises rates because the economy is strengthening, that tends to bode well for many high-yield issuers.

SHORTER DURATION, HIGHER CASH FLOW

So how can investors maximize growth in a rising-rate environment? By seeking out bonds that generate a high amount of income. The more cash flow your portfolio can deliver, the more you’ll benefit.

In our view, a short-duration high-yield strategy can offer a particularly good opportunity to take advantage of rising rates; the quicker the bonds mature, the faster investors can put the proceeds to work in higher-yielding securities.

CREDIT QUALITY STILL MATTERS

There are exceptions, of course, and that’s why investors shouldn’t myopically chase the highest-yielding bonds on offer. High-yield securities are more vulnerable to default than are investment-grade ones. And having grown used to low borrowing costs, some high-yield companies may struggle to raise capital as those costs rise, putting their ability to pay back creditors at risk.

That’s why investors should do their credit homework carefully. Many CCC-rated bonds issued by companies with fragile finances could be vulnerable in a rising-rate environment.

It’s also important to remember that talk of rising rates has made short-duration high-yield strategies popular. That’s another reason why credit quality matters. In our view, investors should be prepared to carry out careful credit analysis on each and every bond before buying.

Investors may also want to look into floating-rate securities, which can benefit in a rising-rate environment. But again, selectivity is important. Bank loans boast floating rates, but most are callable at par, with no penalty for the issuer. That means investors probably won’t always reap the benefits of the floating-rate structure. Credit risk–transfer securities from Freddie Mac and Fannie Mae may be another option.

DON’T SELL YOUR BONDS—IT’LL COST YOU

The biggest mistake investors can make, though, is to try to time the next interest-rate rise or to sell their bonds just as yields start to move higher. Doing so will only lock in losses. And staying out of the market is an expensive proposition. The Fed has repeatedly said it intends to raise rates gradually. Translation: the yield on cash will be only slightly above 0% for some time to come.

When yields are too low, bonds don’t pull their weight in an investment portfolio. When yields hit zero or go negative, as they have in Japan and many European markets, bonds don’t really work at all. That’s why rising rates are a good news.

Will there be more volatile trading ahead? Probably. But investors with a multiyear investment horizon are likely to benefit as rates rise. They can afford to overlook short-term volatility.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.