With all the hazards in the hunt for better retirement outcomes, how can defined contribution (DC) plans improve? As with many other pursuits, what gets measured gets managed…and gets better.

THE LITMUS TEST FOR MEASURING SUCCESS

In our latest survey of DC plan sponsors, we asked sponsors to name their top two critical measures of plan success. The number one response? Employees’ confidence about their prospects for a comfortable retirement.

In fact, the top five answers all related to a common theme: sponsors want employees to understand more and feel better prepared for living in retirement. It’s worth noting that a goal making headlines today—reducing plan fees—was ranked far lower.

Plans have taken several approaches to augment and improve participants’ retirement saving (and confidence):

- Offering financial wellness programs

- Adopting a qualified default investment alternative (QDIA), such as a target-date fund, and implementing a company-wide reenrollment

- Diversifying core-menu bond options with global bonds

- Incorporating some alternatives—possibly using a more sophisticated target-date glide path

- Adopting automatic enrollment and automatic escalation.

As might be expected, more plans that already use auto-enrollment have seen greater increases in plan participation than those that don’t use it. And decreases in plan participation are slightly higher for those without auto-enrollment.

But here’s what’s really interesting: Sponsors of plans that saw declining participation feel even more strongly that “having employees feel confident about their prospects for a comfortable retirement” is a top measure of plan success. Auto-enrollment can move that goal off the wish list and onto the chart of accomplishments.

REBOOTING WITH ROBO-ADVICE

Robo-advisor services are another DC participant-servicing tool. They’ve been around for years, but there’s been a recent explosion of new providers. And these digital investment-advice tools have evolved into a wide spectrum of variations on a common theme of using automated techniques to build and manage portfolios.

Typically based on computer algorithms, robo-advice for DC plans may provide a low-cost level of interactivity for individual participants, regardless of their account balances. It might also be cost-effective to plans by lowering call-center use.

As with financial wellness programs, larger plans have taken the lead in adopting robo-advice—roughly 40% of institutional-size plans use it versus less than 20% of smaller plans. And like plans using wellness programs, more plans offering robo-advice services have seen increases in plan participation over the last three years: 58%, versus 43% of plans without robo-advice.

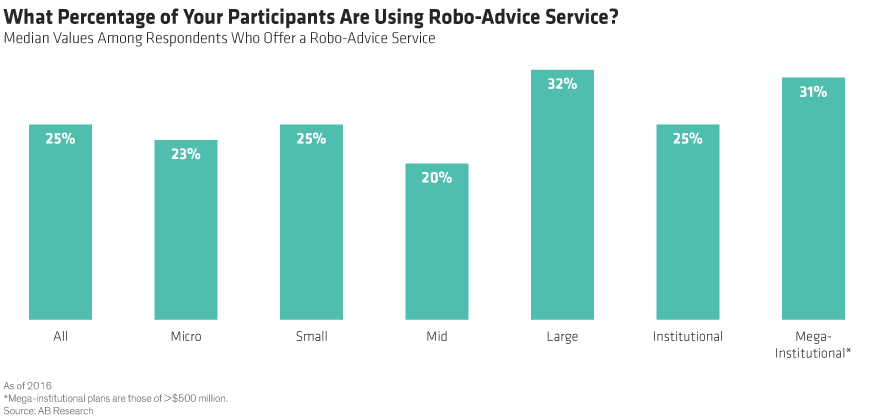

Overall, more than one-fourth of plans (27%) offer robo-advice to their participants. And roughly 25% of participants in these plans access the robo-advice service (Display 1). In addition, about one-fourth of our respondents who don’t currently use robo-advice now say they either are considering it or aren’t sure at the moment.

ADDING A “PERSONAL TRAINER” FOR DC PLAN SPONSORS

But plan sponsors need to feel confident in adding these confidence-building tools, so companies may need to improve their fiduciary training for plan sponsors.

One thing that can help is enlisting the assistance of a financial advisor or consultant (we’ll refer to them collectively as financial advisors). Many larger plans have access to in-house teams as well as additional outside resources. Smaller plans don’t, so the help of a financial advisor can have significant benefits—for plan sponsors as well as participants.

Of respondents whose plans have less than $50 million in assets, over 80% say they use a financial advisor. Nearly as many (73%) say it’s important or very important to them to have a financial advisor act as a fiduciary.

When we ask respondents why, the most frequently cited reason (59%) is to have an objective check on the advice they get from their plans’ other service providers. What plan sponsors value most about using financial advisors is that they provide quality investment advice and guidance (57%). Just over half of sponsors who use financial advisors feel another valuable aspect is that fees are reasonable for the services received.

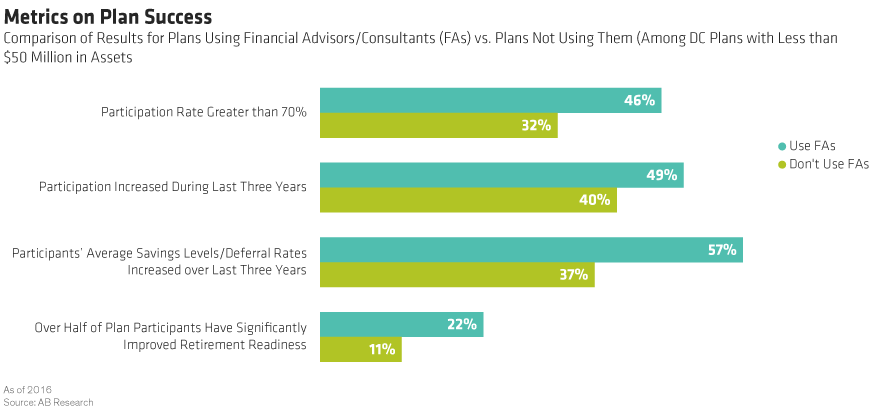

On many metrics for plan success, micro to midsize plans that use financial advisors fare much better than plans that don’t use advisors (Display 2). More plans using advisors show healthy participation rates, increased participation in the last three years, higher average savings among participants and more participants improving their retirement readiness.

In the quest to improve DC plans, plan sponsors are focusing on making participants more confident in their retirement readiness. With new tools and enhanced fiduciary training, we think sponsors will feel more confident that they can raise their plans’ grades.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

"Target date" in a fund's name refers to the approximate year when a plan participant expects to retire and begin withdrawing from his or her account. Target-date funds gradually adjust their asset allocation, lowering risk as a participant nears retirement. Investments in target-date funds are not guaranteed against loss of principal at any time, and account values can be more or less than the original amount invested—including at the time of the fund's target date. Also, investing in target-date funds does not guarantee sufficient income in retirement.