It’s not what you earn, but what you keep after taxes that matters. For many investors, that makes tax-loss harvesting an important part of the picture in enhancing after-tax returns. Harvesting losses involves selling investments that have lost value—whether it’s individual securities or commingled vehicles—in order to offset gains elsewhere in a taxable account.

If investment losses exceed gains at the end of a given year, it’s possible to offset up to $3,000 of non-investment income. That can deliver added tax advantages, especially when an investor’s income tax rate is higher than the capital gains tax rate. If losses are more than $3,000, investors can carry the excess losses forward, using it to offset future capital gains and ordinary income over their lifetimes.

Capital markets have certainly been challenging in 2022, with the S&P 500 down 23% and the Bloomberg Aggregate Bond Index down almost 20% as of October 21. The municipal bond market suffered its worst nine-month start in history.

The market downturn may have a silver lining though: a sizable opportunity to harvest tax losses that can offset future gains. Deferring taxable gains might not be top of mind in 2022, given the heavy losses we’ve seen, but future rebounds could produce gains again. Because tax losses never expire, today’s market offers a potential tax-management tool that could deliver benefits well into the future.

How Tax-Loss Harvesting Has the Potential to Work with ETFs

For many investors, exchange-traded funds (ETFs) have become a valuable tool for reinvesting proceeds from sales that generate tax losses. These vehicles are liquid, can be bought and sold on centralized exchanges, and are tax-efficient. To see how this might work, let’s assume an investor’s portfolio includes a passive ETF that tracks the ICE AMT-Free US National Municipal Index, which has declined 10% so far in 2022.

The investor could sell the passive ETF position, realize tax losses and reinvest the proceeds in a short-duration ETF (such as TAFI, the AB Tax-Aware Short Duration Municipal ETF), keeping muni exposure with less interest-rate risk. Investors have used ETFs to harvest tax losses from mutual funds, too. As per Morningstar 1 , actively managed municipal bond funds have seen over $63 billion in net outflows as of July this year, with ETFs seeing more than $13 billion in inflows.

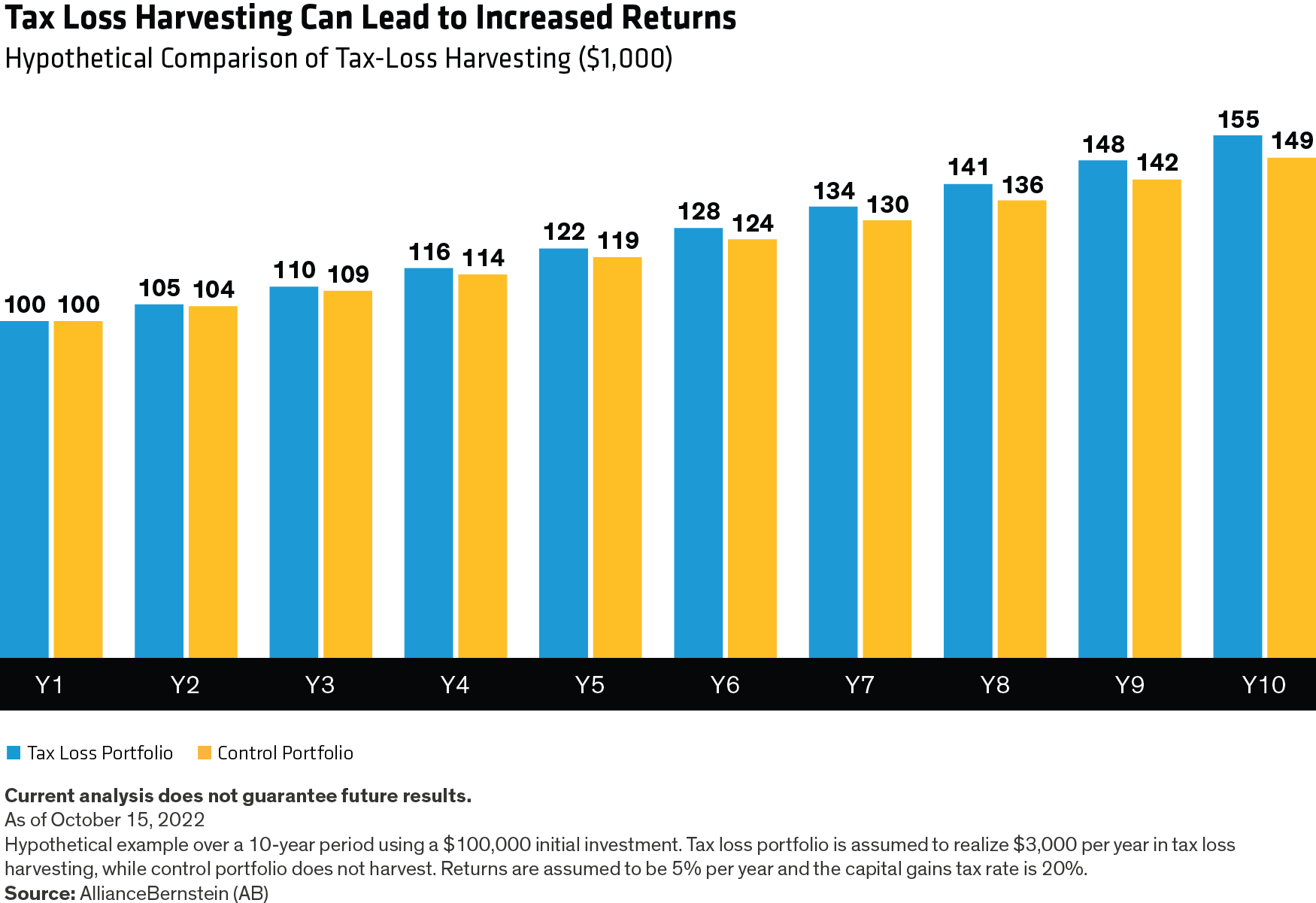

A Simple Example: How Harvesting Losses Can Add Up

Over time, the benefits of effective tax-loss harvesting can be significant. We can look at the impact with a simple example using two portfolios with an initial $100,000 investment, each generating a 5% return per year over 10 years. The tax-loss portfolio realizes $3,000 per year in tax-loss harvesting benefits, while the control portfolio does not.

Based on an assumed capital gains tax rate of 20%, the tax-loss portfolio would end the 10-year period with a value of approximately $155,000, significantly higher than the roughly $149,000 for the control portfolio, which doesn’t employ tax-loss harvesting ( Display 2 ). That advantage translates into a cumulative total-return advantage of 4.5%.

Potential Wash-Sale and Other Benefits from ETF Structures

In addition to maintaining market exposure, tax-loss harvesting that involves buying an ETF may avoid violating the wash-sale rule, which prevents investors from claiming losses on the sale of an investment if they buy an identical one within 30 days. The ETF wrapper is also well-suited to taxable accounts, because it offers benefits versus mutual funds, including:

- Because ETFs are exchange traded, ETF investors may be insulated from individual investors’ trading. So, if an investor decides to sell shares of an ETF, the transaction will usually happen in the secondary market, which doesn’t impact the ETF itself.

- When selling on exchange does result in a redeeming of ETF shares, it’s usually tax-free to remaining investors. That’s because redeeming in kind involves ETFs merely being unwrapped from the underlying securities.

A Potential Strategy for Employing Tax-Loss Harvesting

How might tax-loss harvesting play out in the real world today? We’re witnessing a “safety dance” by many investors during 2022 into short-duration bond strategies as interest rates remain upward-bound. Over $30 billion has moved into ultra-short ETFs as of September, according to Morningstar 3 .

With higher yields offering a much more enticing proposition for these strategies and given their low duration profiles, investors have an opportunity to rebalance their portfolio’s risk profiles while preserving income-generating potential. For investors seeking to accrue losses before year end, AB’s short-duration ETFs could be a natural home for tax-loss proceeds.

For a strategy that helps limit duration risk with a focus on after-tax return and income, consider AB Tax-Aware Short Duration Municipal ETF (TAFI) . For more information on AB’s ETFs, visit www.ABFunds.com/go/ETFs .

Not to be treated as tax advice. Please speak with a professional tax advisor.

Investing in ETFs involves risks, including loss of principal.

Investors should consider the investment objectives, risks, charges and expenses of the Fund/Portfolio carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at abfunds.com or contact your AB representative. Please read the prospectus and/or summary prospectus carefully before investing.

TAFI—Bond Risk: The Fund is subject to the same risks as the underlying bonds in the portfolio, such as credit, prepayment, call and interest-rate risk. As interest rates rise, the value of bond prices will decline. Below-Investment-Grade Securities Risk: Investments in fixed-income securities with lower ratings (aka “junk bonds”) are subject to a higher probability that an issuer will default or fail to meet its payment obligations. These securities may be subject to greater price volatility due to such factors as specific municipal or corporate developments and negative performance of the junk bond market generally, and may be more difficult to trade than other types of securities. Municipal Market Risk: Economic conditions, political or legislative changes, public health crises, uncertainties related to the tax status of municipal securities or the rights of investors in these securities may negatively impact the yield or value of a municipal security. Tax Risk: The US government and Congress may periodically consider changes in federal tax law that could limit or eliminate the federal tax exemption for municipal bond income, which would in effect reduce the income shareholders receive from the Fund by increasing taxes on that income. Derivatives Risk: Derivatives may be more sensitive to changes in market conditions and may amplify risks. New Fund Risk: The Fund is recently organized, giving prospective investors a limited track record on which to base their investment decision.

The S&P 500 Index is a stock market index tracking the stock performance of 500 large companies listed on stock exchanges in the United States. The Bloomberg US Aggregate Bond Index is a broad base, market capitalization-weighted bond market index representing intermediate term investment grade bonds traded in the United States. The ICE AMT-Free US National Municipal Index measures the performance of investment-grade municipal bonds that are exempt from U.S. federal income tax and the Alternative Minimum Tax (AMT). Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

AllianceBernstein ETFs are distributed by Foreside Fund Services, LLC, in the US only.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

© 2022 AllianceBernstein L.P., 501 Commerce Street, Nashville, TN 37203

RMT-308046-2022-10-11

1 Morningstar Direct as of July 31, 2022

2 The example used is hypothetical and not representative of any actual investment. In 2022, a 20% capital gains tax rate is applicable to persons with a total taxable income as follows: a single person with >$459,750; married filing separate >$258,600; head of household >$488,500; and married filing jointly >$517,200. Lower taxable income would have a lower capital gains tax rate. No state capital gains tax is assumed in this example.

3 Morningstar Direct as of September 30, 2022