-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Eurozone Banks

Is There Life After TLTRO?

21 November 2018

4 min read

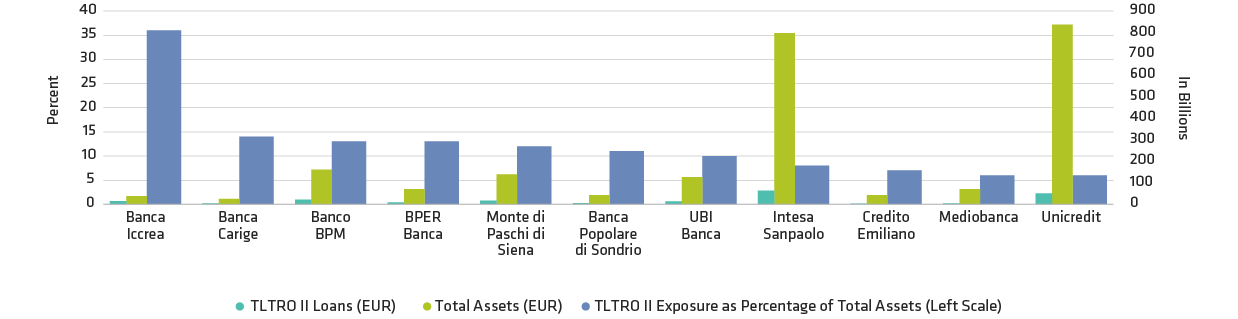

Italian Banks’ Exposure to TLTRO II

Second and Third Tier Banks Are Most Exposed Relative to Their Total Assets

As of 31 December 2017

Banks shown are a sample set of TLTRO II borrowers and not a comprehensive listing of all Italian banks.

Historical and current analyses are for informational purposes only.

Source: Individual banks’ reporting

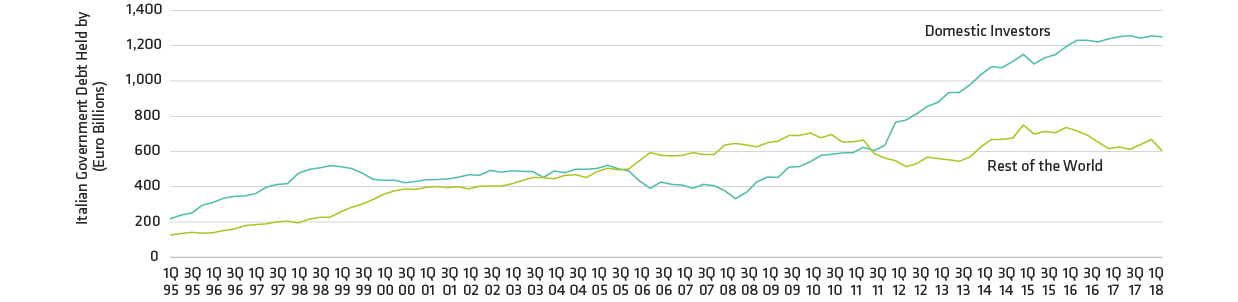

Italian Government Debt Is on the Rise

But Foreign Investors Are Reluctant to Buy

As of 30 June 2018

Historical and current analyses are for informational purposes only.

Source: Haver Analytics (Italian National Accounts)

Valuations Have Become More Attractive

AT1 Spread Has Widened 85% Since the Tights of 2018, and Is Now Close to the Historical Average

As of 15 November 2018

Historical and current analyses are for informational purposes only.

Source: Bloomberg Barclays

-

AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

About the Author