-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

Equity Market Sell-Off

Return to Reality?

12 February 2018

4 min read

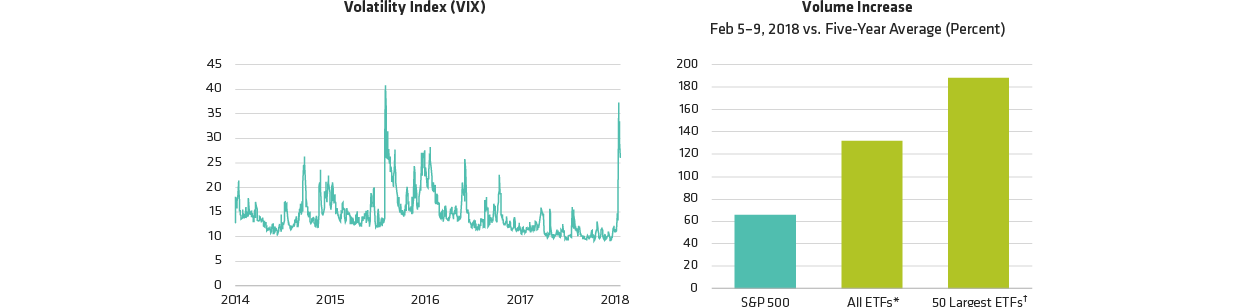

Volatility and Volumes Spiked Sharply After Prolonged Period of Market Calm

As of February 9, 2018

Past performance and current analysis do not guarantee future results.

*Based on 1,436 US-listed ETFs with assets under management (AUM) greater than US$25 million

†Largest ETFs by AUM

Source: Bloomberg, Chicago Board Options Exchange, Morningstar Direct, S&P and AllianceBernstein (AB)

After Sharp Downturn, Stocks Are Down Modestly This Year

Index Returns (Total Returns, USD)

As of February 9, 2018

Past performance and current analysis do not guarantee future results.

US large-caps represented by S&P 500, global stocks by MSCI World, international stocks by MSCI EAFE, emerging-market stocks by MSCI Emerging Markets, European stocks by MSCI Europe and US small-caps by Russell 2000

Source: Morningstar Direct, MSCI, S&P and Russell Investments

US Equity Valuations Have Fallen Substantially

S&P 500 Index: Price/Forward Earnings (Next 12 Months)

As of February 9, 2018

Past performance and current analysis do not guarantee future results.

Source: FactSet

About the Authors