-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

How to Invest in Equities When Guidance Disappears

01 May 2020

4 min read

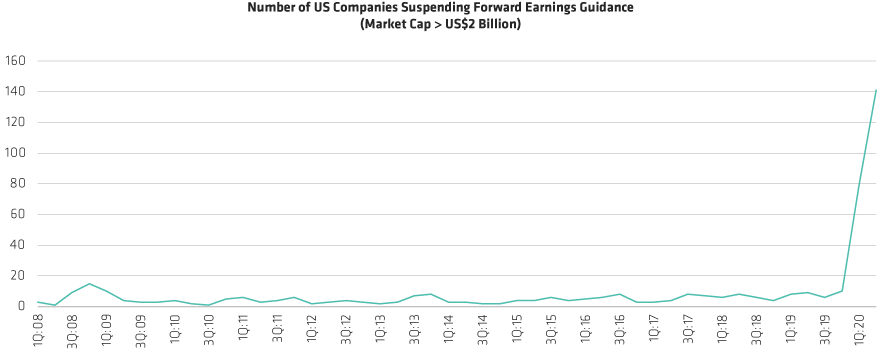

US Companies Are Suspending Guidance in Unprecedented Numbers

Through April 29, 2020

Based on US Companies that have filed an 8-K form, used to notify shareholders of an unscheduled material event that could be of importance to investors.

Source: AlphaSense, company filings and AllianceBernstein (AB)

Earnings Estimates: Wide Dispersion and Short-Term Horizon

Historical performance and current analysis does not guarantee future results.

Left Display through March 31, 2020; right chart through April 21, 2020

*Based on FactSet annual earnings estimates. Dispersion is calculated by taking the standard deviation of earnings estimates for every stock over the last 100 days, divided by the absolute value of each stock’s median earnings estimate, multiplied by 100. For every period shown, the median dispersion value is used.

Source: FactSet, S&P and AllianceBernstein (AB)

About the Authors