-

The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer of solicitation for the purchase or sale of, any financial instrument, product or service sponsored by AB or its affiliates.

Plan Sponsors Speak with Action

October 26 2018

3 min read

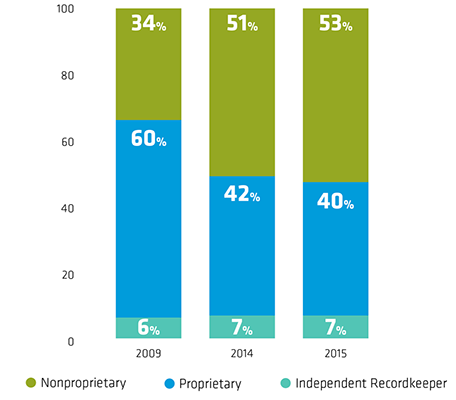

1. Recordkeepers’ proprietary TDF share has declined by 20% since 2009, as the use of nonproprietary TDFs has increased by 19%. Both of These numbers are up from the last study.

Recordkeepers’ Target-Date Assets (Percent)

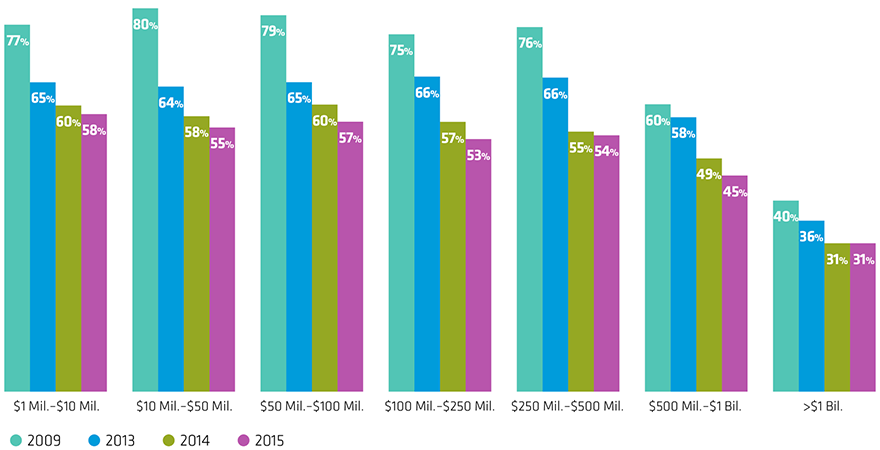

2. More smaller plans (53%) use record keeper proprietary TDFs. Usage among large1 plans is much lower (31%), because “unbundling” of target-date decisions from plan administration decisions is more common.

Assets by Plan Size (Percent)

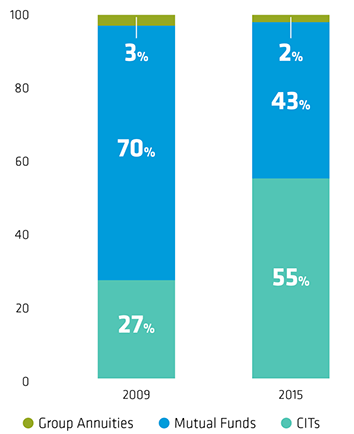

3. The use of collective investment trusts (CITs) in TDFs has jumped since 2009, with some recordkeepers using CITs or passively managed TDFs to reduce fees and keep their proprietary share.

Target-Date Assets by Vehicle (Percent)