Oil and gas producers are often seen as vulnerable to global efforts aimed at curbing climate change. But some European energy groups might become part of the solution to climate change rather than part of the problem.

The Climate Change Investing Challenge

Energy companies’ operations raise several important environmental, social and governance (ESG) concerns. Extracting and producing oil and gas is carbon-intensive, while the polluting effects of oil spills and the risk of contributing to corruption in oil-producing countries are additional ESG risks.

Most major energy companies have raised their game in these areas in recent years. But the most pressing ESG issue for investors is climate change, since carbon-based fuels are a major source of CO2 emissions. There are two big issues for oil and gas companies: are their businesses sustainable in the long run, given the need to move to lower carbon energy sources? And are they doing enough to reduce the carbon emissions that they and their products produce?

Gauging the Risk of Stranded Assets

To answer the first question requires an understanding of how investors value energy companies’ assets and the cash flows they produce. Our research suggests that some European integrated oil companies currently trade at valuations that don’t fully reflect their discovered commercial reserves—oil and gas already connected to distribution infrastructure or which can be economically developed. In other words, investors are not ascribing value to future reserves whose long-term commercial potential is highly uncertain.

Could the discovered commercial reserves become “stranded”? If so, shareholders would have paid for assets without any commercial value as the role of carbon-based energy sources in the global economy diminishes.

Probably not. Take Repsol and Total, for example. Repsol has commercial reserves (proven plus unproven) which would last 18 years in total. However, our analysis suggests that the current share price only reflects cash flows from oil production for about half of this period. Total’s corresponding oil reserves should last 26 years, which presents more risk. But a similar analysis implies that the current share price assigns no value to the company’s oil production potential beyond 11 years from now.

This means that investors are taking a clear-headed view of the long-term challenges to oil production. Projected changes in fuel use suggest that oil demand will peak in the 2030s. This is based on expected efforts to meet targets for limiting the rise in global temperature agreed in the Paris Climate Change Convention. Of course, this depends on governments accelerating efforts to encourage renewable power and electric vehicles. Even after the peak, forecasters see oil products remaining in strong demand for several decades, particularly for aviation and marine fuels and petrochemicals. These trends—coupled with our valuation analysis above—suggest that shareholders of oil producers today are unlikely to see the current value of their investments wiped out by moves to meet the Paris goals.

Steps Towards Transformational Change

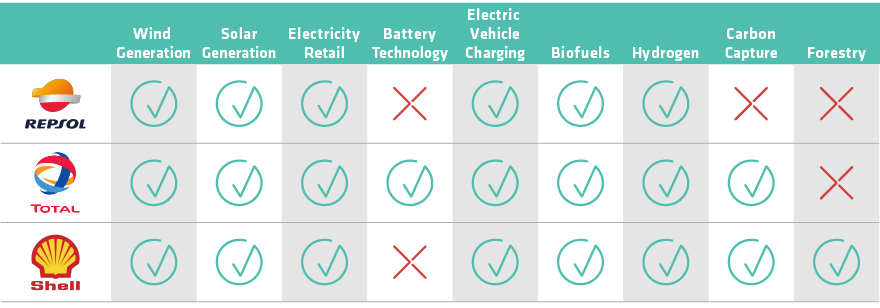

But are those producers unavoidably part of the climate change problem or can they be part of the solution? The answer depends on the nature of the commitments and changes that individual companies are making. Most major energy companies are taking effective steps to reduce the carbon emissions produced by their own activities, for example, when extracting or transporting oil and gas. But only a few—notably Repsol, Shell and Total—have also committed to reduce average emissions from the use of their products in transport, industry and other areas, to meet the Paris goals.