-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

Are Low-Volatility Stocks Too Expensive?

Jan 17, 2020

3 min read

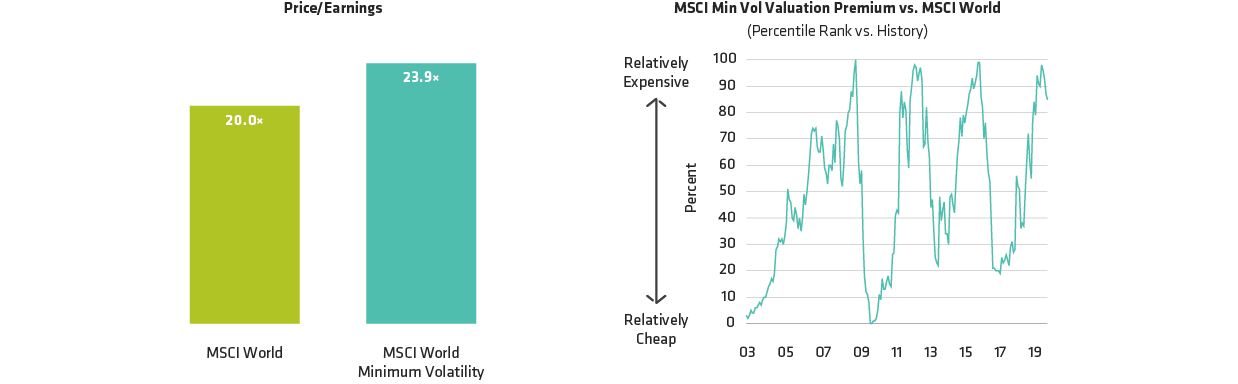

Valuations of Lower-Volatility Stocks Look Relatively High

Historical and current analyses do not guarantee future results.

As of December 31, 2019

Source: FactSet, MSCI and AllianceBernstein (AB)

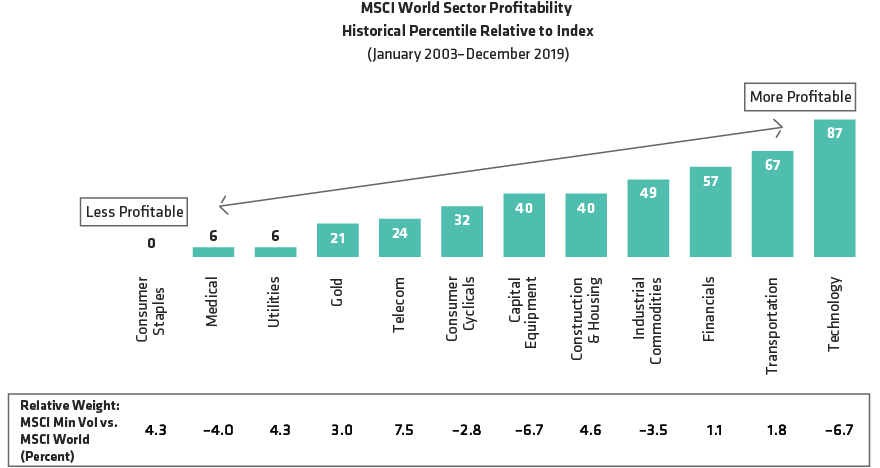

Look for Quality Across Sectors to Find Good Value

Historical and current analyses do not guarantee future results.

As of December 31, 2019

Source: FactSet, MSCI and AllianceBernstein (AB)

About the Authors