If funding is available, what keeps companies from spending more? Many companies don’t have enough good ideas to fund, while others lack vision. Bureaucratic governance structures may also hinder timely investment. Of course, tax reform could spur companies to launch new investment initiatives. However, many companies strive to grow earnings annually, which can also influence how they prioritize capital allocation and detract from their ability to sustain future profitability. In our view, many companies might be choosing not to fund good ideas because it’s simply easier to buy back stock, which flatters short-term EPS growth rates.

What’s wrong with that? The challenge is that maintaining high profitability often requires an intelligent trade-off between managing expenses while funding business model improvements and future growth opportunities.

Sustained investment is always vital to future shareholder value creation—especially in a world that’s rife with technological disruption. That’s why we believe investors should scrutinize companies for signs of underinvesting. Companies that underinvest might look healthy today, but their high margins may mask an underlying weakness: a lack of readiness for looming threats to a business model.

The Investor’s Dilemma: Is High Profitability Good or Bad?

This presents a conundrum for investors. High profitability, typically measured by margins, is usually seen as an attractive trait in a company. So how can you know when it’s really an Achilles’ heel? We think the following signs of underinvestment can help investors distinguish between companies with sustainably high profitability and high-risk companies with limited reinvestment opportunities:

- Declining R&D or selling expenses—in absolute terms or as a percent of revenue, suggest that a company may be too focused on short-term margins at the expense of the future

- Rising talk of “targeted investments”—especially in combination with declining spending levels, is often an implicit admission that a company is actively choosing not to invest in potential opportunities. Such narrow, tactical moves afford less tolerance for an investment miss. Don’t be fooled by the jargon.

- Slow organic sales growth—especially if it lags peers, could indicate that a company’s core current product lines are falling behind and require increased future investment

- Acquisition fever—is perhaps the biggest and most damaging sign of cumulative underinvestment. A company on a buying spree may be trying to catch up with peers. While some takeovers help a company improve its market position, they can be a sign that the company is underinvested in key markets, made the wrong investments, or both. In extreme cases, acquisition fever could signal that a company is lacking innovation or has damaged governance.

Takeovers generally demonstrate clear strategic intent and are accretive to earnings. But investors tend to focus too much on earnings accretion and too little on return on invested capital (ROIC)—an important driver of stock returns, in our view. The expected long-term benefits of acquisitions don’t always materialize and the high premiums typically paid for deals often structurally dilute ROIC, especially compared to organic investment.

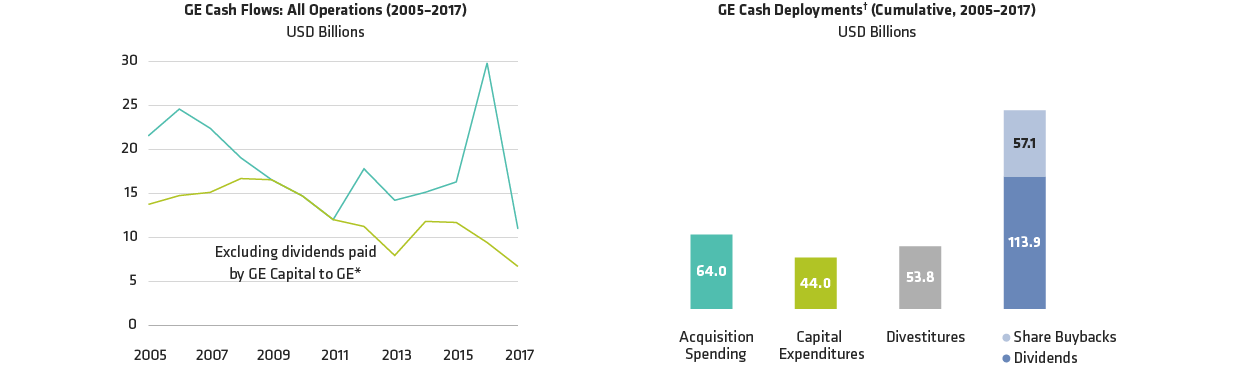

GE’s Breakup Reflects Cumulative Investment Missteps

GE’s recent decision to break itself up into three fully separate, more focused companies presents an excellent example. Since 2005, the company spent $64 billion on acquisitions designed to reposition itself (Display). It also returned a net $171 billion to shareholders since 2005. Much of it was funded by liquidations at GE Capital.