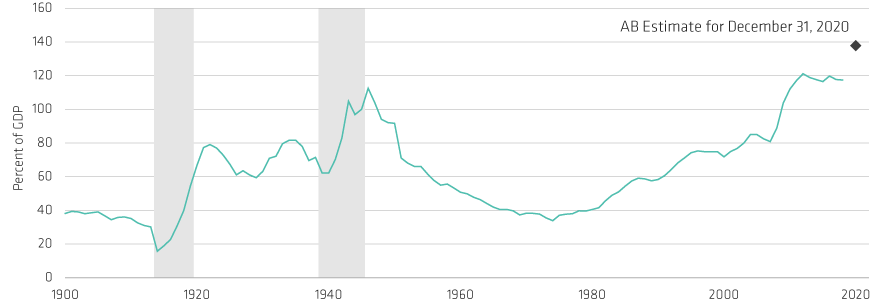

According to our simulation, DSIRs range from a high of 1.7% in Germany to –1.1% in the UK, –1.3% in the US and –1.5% in France. This doesn’t mean the US will push its policy rate into negative territory—indeed, we continue to think that unlikely. But it does mean that government debt will move onto an explosive path unless the average cost of funding is kept very, very low—particularly in countries with negative DSIRs. And that’s where central banks come in.

In recent weeks, many central banks have either launched, reopened or expanded large-scale government-bond purchase programs. This is similar to the GFC policy response but there are key differences. The coronavirus crisis response has been faster and broader: the US Federal Reserve bought $1.5 trillion of Treasury debt in March and April, something that took four years to accomplish during the GFC. And we expect much more to come. The goal is different, too: central banks now talk much more openly about the link between their purchases and government financing costs.

Fiscal and Monetary Policy Joined at the Hip

Very few central bankers would be willing to admit that they are monetizing government deficits. But that’s exactly what they are doing and, more importantly, it’s precisely what they should be doing in current circumstances. Just as during wartime, central banks currently have little option but to step into the nexus that blurs the distinction between monetary and fiscal policy, with the two effectively joined at the hip.

In time, governments and voters will have to decide how best to deal with very high levels of public sector debt. Default, austerity and higher inflation are among the possible options. Alternatively, they could choose to downplay the significance of government debt, as some advocates of modern monetary theory would recommend. But those are questions for another day. And until then, what’s important is that interest rates and bond yields remain low.

In recent weeks, central banks have clearly shown that they have both the ability and the willingness to keep a lid on bond yields. So at a time when the global outlook is subject to so many uncertainties, our highest-conviction view is that interest rates and bond yields will continue to be pinned close to, and in some cases below, zero. And that’s likely to be the case long after the coronavirus crisis has passed.

*The G7 is Canada, France, Germany, Italy, Japan, the UK and the US.