Rising interest rates make bond investors nervous. But purging your portfolio of interest-rate risk can backfire—even in a rising-rate environment. There’s a better way to balance risk and return.

As we noted in a previous blog, we’ve found that investors can minimize risk and earn relatively high income by pairing rate-sensitive assets such as government bonds with growth-oriented credit assets in a single portfolio and letting their managers adjust the balance as conditions change.

A key benefit of this approach, known as a credit barbell strategy, is that it helps investors avoid leaning too far in either direction—and overexposing themselves to a single risk.

For example, when investors see bond yields rise as sharply as US Treasury yields did between November and March, they often do the following two things:

First, they reduce duration—or interest-rate risk—in their core bond portfolios, which focus on investment-grade debt and include a healthy share of government bonds. Higher rates reduce the market value of these securities.

Second, they take more credit risk in their high-income allocation, as high-yield bonds, emerging-market debt and other credit assets tend to outperform when growth and interest rates rise.

Rising Rates Don’t Have to Derail Returns

US bond yields’ upward momentum has stalled recently. But let’s face it: if the economy keeps improving, the Federal Reserve will keep raising rates and yields will probably resume their climb. If the European Central Bank ends quantitative easing later this year, European yields may rise, too.

In other words, expect plenty of investors to stick to the script.

Here’s the problem: cutting back too drastically on interest-rate-sensitive assets such as Treasuries or mortgage-backed securities can make a fixed-income allocation less diverse—and less stable.

It can also cost investors income. Sure, government bonds, mortgage-backed securities and even many investment-grade corporate bonds are highly sensitive to rising interest rates. But as these bonds mature, their prices drift back toward par. That means investors can reinvest the coupon income in newer—and higher-yielding—bonds.

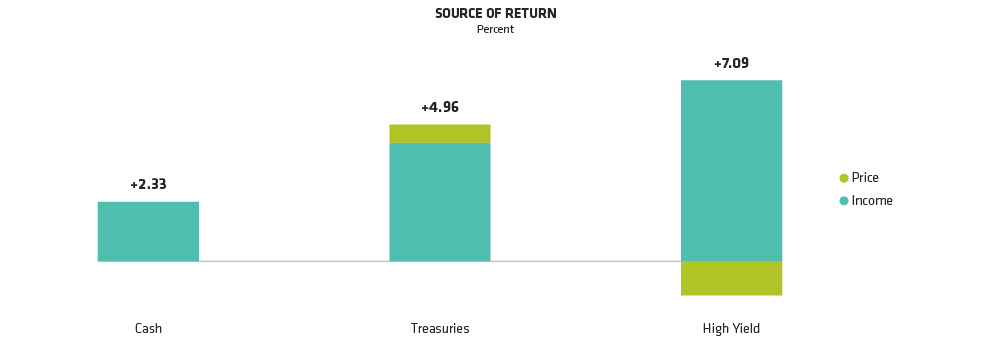

As the Display below shows, income accounted for nearly all the average quarterly return of US Treasuries over the last 20 years—a period when yields fell sharply and prices rose. High-yield bonds, of course, relied even more heavily on income to drive returns—price movement was a negative.