-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

US Corporate Cash Is Down

Should Investors Worry?

Jul 23, 2019

3 min read

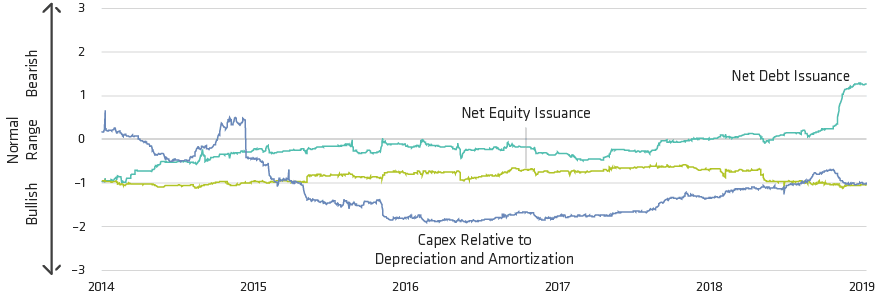

Net-Debt Issuance Indicator Is Flashing a Warning

Z Scores for Equity-Quality Indicators

Data presented as z scores, a standardized measure that indicates how many standard deviations an indicator is from the mean. Higher z scores indicate a bearish signal while lower z scores indicate a bullish signal. Net equity issuance equals the change in common shares outstanding, the log of (common shares outstanding (t)/common shares outstanding (t–1)). Net debt issuance equals the change in (total debt minus cash) divided by average total assets. Total debt equals long-term debt plus debt in current liabilities plus preferred stock capital plus noncontrolling interest. Cash equals cash plus short-term investments.

As of July 11, 2019

Source: S&P Compustat and AllianceBernstein (AB)

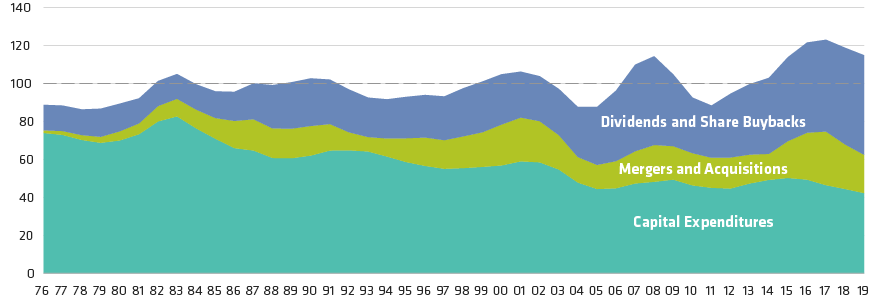

Trends in Corporate Cash Usage

Percent of Gross Cash Flow (Three-Year Rolling Average)

As of June 30, 2019

Source: FactSet and AllianceBernstein (AB)

About the Authors