The active/passive debate has been raging for years, and both approaches have merit. But there’s more to the story than meets the eye. Investors who commit too much to passive—and not enough to active—could face mounting risks.

No one disputes that passive investing plays an important role in many investors’ portfolios—especially over the past decade. Passive strategies open the door to low-cost market access. But passive’s explosive growth is creating a buildup of structural challenges, just as active investing faced structural challenges in its heyday.

Today, roughly 1,800 exchange-traded funds (ETFs) are chasing less than half that number of US stocks with a market cap over $5 billion. ETF growth doesn’t look to be slowing down, and crowding in certain stocks and market segments is likely to intensify. As investors have piled into passive spaces, specific distortions have begun to form, with the most passively held stocks becoming more volatile and more highly correlated to each other versus the broad market. And both measures seem to be intensifying.

In our view, four factors collectively magnify the risks to investors:

- Crowding. Investors who follow the herd when making portfolio decisions tend to pile into certain stocks and market spaces. The following three factors make crowding worse.

- Fragility. Investors in a specific market segment or trade usually expect a certain outcome. And they’ll quickly jump ship if they don’t see the results they want. Think of it as collective flight risk.

- Liquidity. Crowds in a panic run for the exits, creating a liquidity crunch. If liquidity is drying up, how hard will it be to find a door? And how much will passive investors have to pay to open one?

- Passive Ownership. If passive investors in an ETF want out of a crowded trade, they have to sell the entire index, regardless of individual stocks’ merits. It’s like selling the baby with the bathwater.

What Happens When Crowded Trades Break?

February’s equity market correction gave us a prime example of what happens when too many investors are pouring too much money into a passive trade that falls apart.

When the CBOE VIX—a well-known gauge of market volatility—fell to near-record lows recently, many investors took short positions in the VIX. Essentially, they were betting that volatility would stay low for a while. But the equity market stumbled, volatility surged and the VIX quadrupled in a week. Passive investments that were short the VIX were hit hard.

Crowding isn’t restricted to more exotic trades like shorting the VIX. In 2015, we saw a widespread equity sell-off in healthcare stocks driven by concern over drug pricing. And a year later, high-yield bond markets reeled after oil and gas prices plummeted. Investors who had crowded into high-yield energy bonds panicked and rushed for the exits. It was hard—and pricey—to get out.

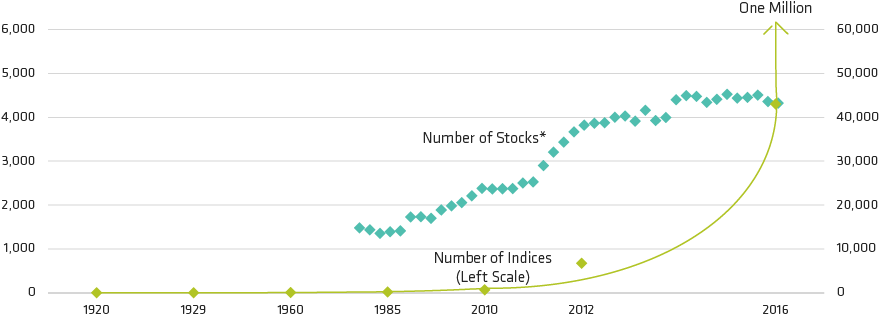

And the risks of passive investment continue to grow. Since passive investments replicate indices, the index business is now booming. By some estimates, there are more than one million indices today (Display)—most of them equity. And we’ve seen more passive vehicles being created to buy stocks to replicate those indices.