-

Past performance does not guarantee future results.

Into the Unknown

Positioning Portfolios for an Unpredictable World

14 September 2018

4 min read

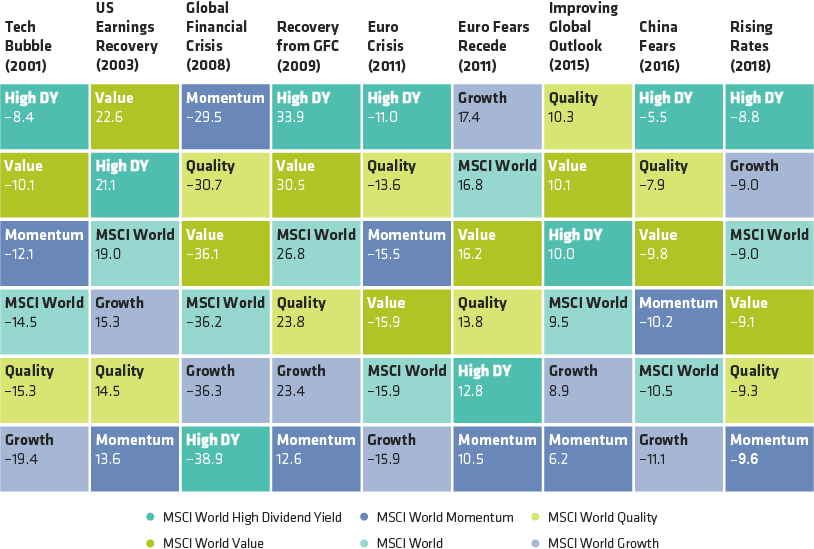

Factor Performance Can Swing Sharply When Markets Are Surprised

Global Factor Index Returns During Major Market Downturns and Recoveries*

As of August 31, 2018

Historical analysis for informational purposes only.

*Based on largest index moves when one or more factors rose or fell by at least 10% from January 1, 2000 to August 31, 2018. Dates for market events listed are: Tech Bubble, February 4, 2001 to March 17, 2001; US Earnings Recovery, March 28, 2003 to June 17, 2003; Global Financial Crisis, September 28, 2008 to November 22, 2008; Recovery from GFC, March 31, 2009 to June 11, 2009; Euro Crisis, July 24, 2011 to August 20, 2011; Euro Fears Recede, October 4, 2011 to October 28, 2011; Improving Global Outlook, September 29, 2015 to October 23, 2015; China Fears, January 3, 2016 to February 13, 2016; Rising Rates, January 25, 2018 to February 2, 2018.

Source: MSCI and AllianceBernstein (AB)

-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

-

Alpha, often considered the active return on an investment, gauges the performance of an investment against the market and is used as a measure of manager skill.

-

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

-

Source: MSCI and AB

About the Authors