-

For investment professional use only. Not for inspection by, distribution or quotation to, the general public. INVESTMENT RISKS TO CONSIDER

The value of an investment can go down as well as up and investors may not get back the full amount they invested. Capital is at risk. Past performance does not guarantee future results.

The Retirement Bridge Funds are available as default investment funds through UK registered pension savings schemes and seek to meet the requirements of a broad range of persons. They do not take into account an individual’s personal circumstances and may not be suitable for a particular individual or group of individuals with complex financial or personal circumstances.

Some of the principal risks of investing in Retirement Bridge Funds include:

Market Risk: The market values of the Fund’s holdings rise and fall from day to day, so investments may lose value. Interest Rate Risk: Bonds may lose value if interest rates rise or fall—long-duration bonds tend to rise and fall more than short-duration bonds. Credit Risk: A bond’s credit rating reflects the issuer’s ability to make timely payments of interest or capital—the lower the rating, the higher the risk of default. If the issuer’s financial strength deteriorates, the issuer’s rating may be lowered and the bond’s value may decline. Allocation Risk: Allocating to different types of assets may have a large impact on returns if one of these asset classes significantly underperforms the others. Foreign Risk: Investing in non-UK assets may be more volatile because of political, regulatory, market and economic uncertainties associated with them. These risks are magnified in assets of emerging or developing markets. Currency Risk: If a non-UK asset’s trading currency weakens versus sterling, its value may be negatively affected when translated back into sterling terms. Reinsurance Risk: The underlying fund(s) is accessed via another insurance provider, also known as a reinsurance arrangement; creating a direct counterparty exposure. In the event of default by an insurance provider, the value of the assets will likely fall, which will be reflected in the value of our Fund price.

Important Information

The views and opinions expressed in this document are based on our internal forecasts and may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice or an invitation to purchase any security or other investment. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This document is not an advertisement and is not intended for public use or additional distribution.

The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. AllianceBernstein L.P. makes no guarantees or representations as to, and shall have no liability for, any electronic content delivered by any third party, including, without limitation, the accuracy, subject matter, quality or timeliness of any electronic content.

Retirement Bridge is available as a default investment fund through UK registered pension savings schemes and seeks to meet the requirements of a broad range of persons. They do not take into account an individual’s personal circumstances and may not be suitable for a particular individual or group of individuals with complex financial or personal circumstances.

Note to UK Readers: This document is issued by AllianceBernstein Limited, 50 Berkeley Street, London W1J 8HA, a company registered in England under company number 2551144. AllianceBernstein Limited is authorised and regulated in the UK by the Financial Conduct Authority (FCA – Reference Number 147956).

The [A/B] logo is a service mark of AllianceBernstein and AllianceBernstein® is a registered trademark used by permission of the owner, AllianceBernstein L.P.

© 2022 AllianceBernstein L.P

Can Your Pension Cope with Inflation Risk?

June 27 2022

8 min read

HOW DAMAGING HAS INFLATION HAS BEEN IN THE UK?

Pound Sterling a Suspect Store of Value 1949

Historical analyses do not guarantee future results.

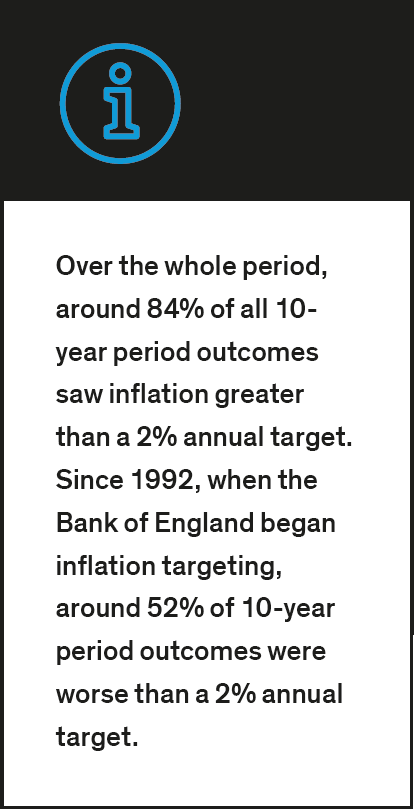

Each line represents the real value of an initial £100 over rolling annual 10-year periods between 1949 and 2022. For example, the first period is the change in £100 between 1 May 1949 and 30 April 1959. Next is between 1 May 1950 and 30 April 1960. The last period is between 1 May 2012 and 30 April 2022. Note that the Bank of England started targeting inflation (equivalent to a 2% level of CPI) in 1992 and rolling periods for which these targets are applicable have been marked in a darker grey.

As of 30 April 2022. Source: ONS and AB