-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

Can Value Stocks Recover Without Help from Financials?

11 August 2020

4 min read

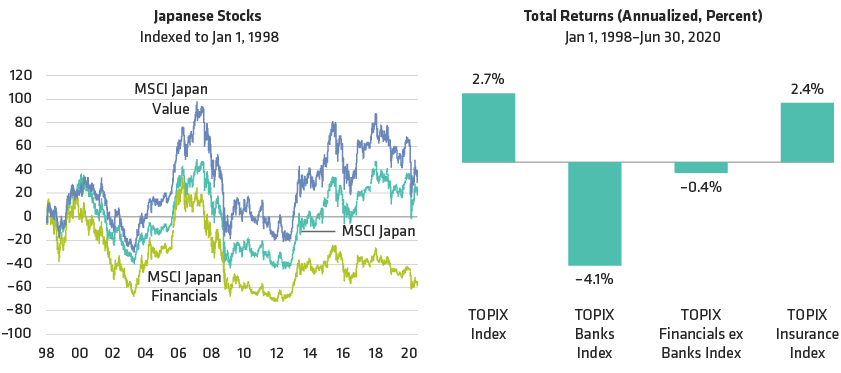

Japanese Value Stocks Have Outperformed Without Financials

Past performance does not guarantee future results.

As of July 31, 2020

MSCI index data is used in left display because the MSCI Japan Value has a longer history than TOPIX Value. TOPIX data is used in right display because it provides financial sub-industry classifications, which are not available for the MSCI Japan index.

Source: Bloomberg, MSCI, TOPIX and AllianceBernstein (AB)

Which Sectors Have Driven Strong Value Equity Markets?

Periods of Sector Outperformance When Value Outperforms (1995–2020)

Past performance and current analysis do not guarantee future results.

As of June 30, 2020

Bar chart shows the number of years that each sector outperformed when MSCI World Value outperforms MSCI World. Average outperformance shows the average annual outperformance of the sector when MSCI World Value outperforms MSCI World.

Shaded boxes refer to sectors that delivered stronger returns than financials on average in years when value stocks outperformed the market.

Source: MSCI, FactSet and AllianceBernstein (AB)

-

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

About the Authors