-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

Does Sustainable Investing Constrain a Portfolio?

13 August 2019

5 min read

Sustainable Companies Can Be Found Across Sectors and Regions

Current analyses do not guarantee future results.

*Sector weightings will vary over time.

As of January 31, 2019

Source: Bloomberg, MSCI and AB

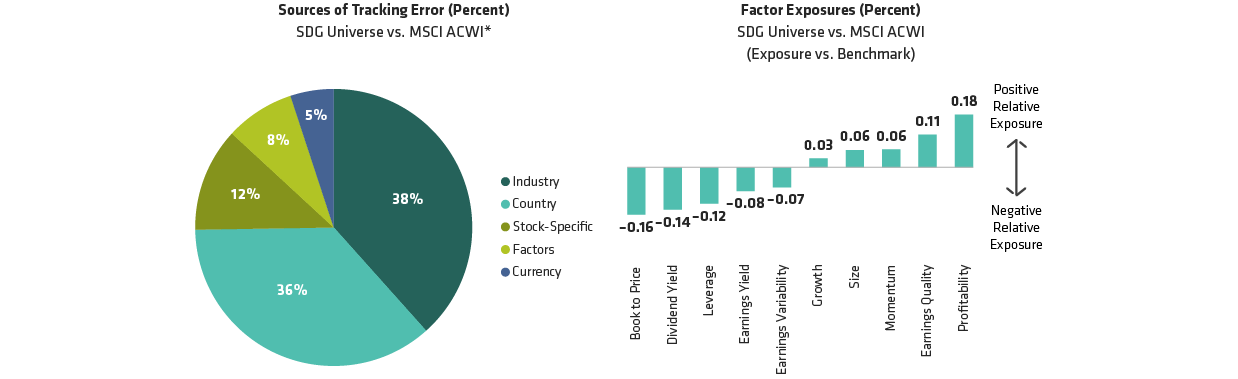

Sustainable Portfolios Tend to Tilt Toward Certain Factors and Sectors

Current analyses do not guarantee future results.

*Numbers may not sum due to rounding.

As of March 6, 2019

Source: Barra, MSCI and AB

-

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

About the Author