-

The views expressed herein do not constitute research, investment advice or trade recommendations, do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

Global Macro Outlook: Fourth Quarter 2024

October 04 2024

1 min read

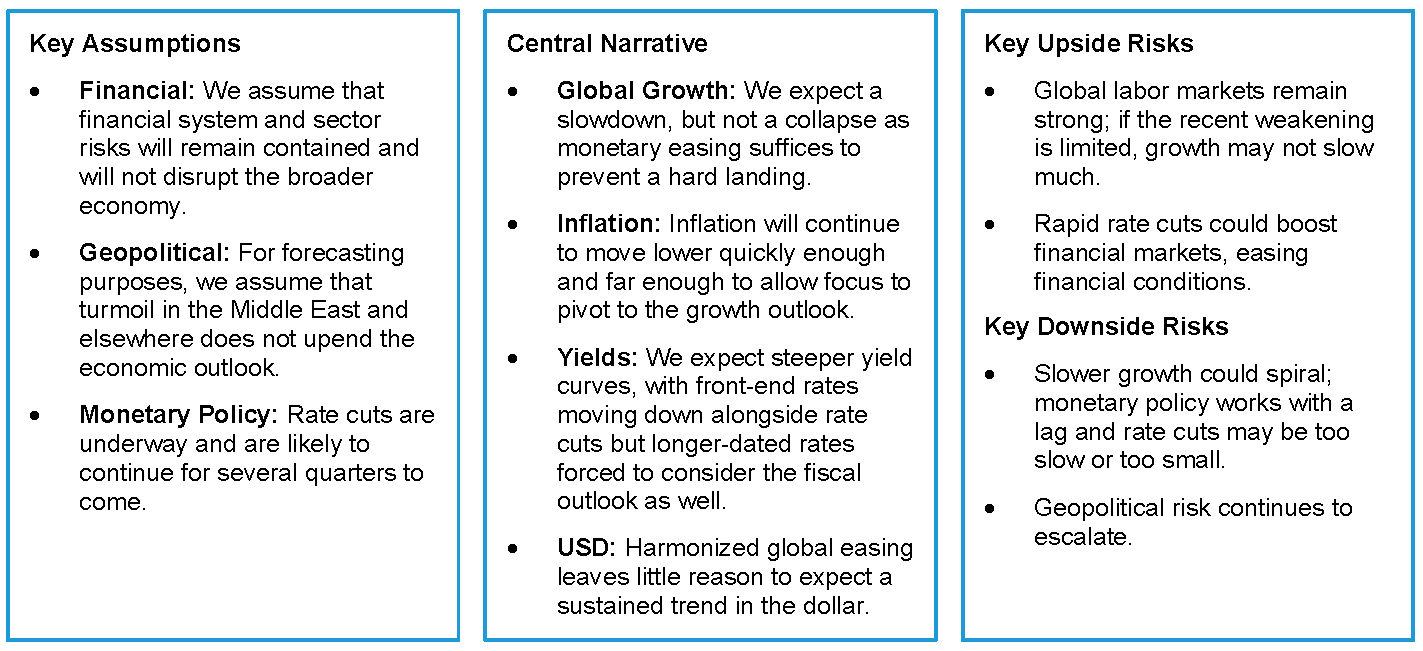

Key Forecast Trends

Global Macro Outlook: The Next Six Months

Global Forecast

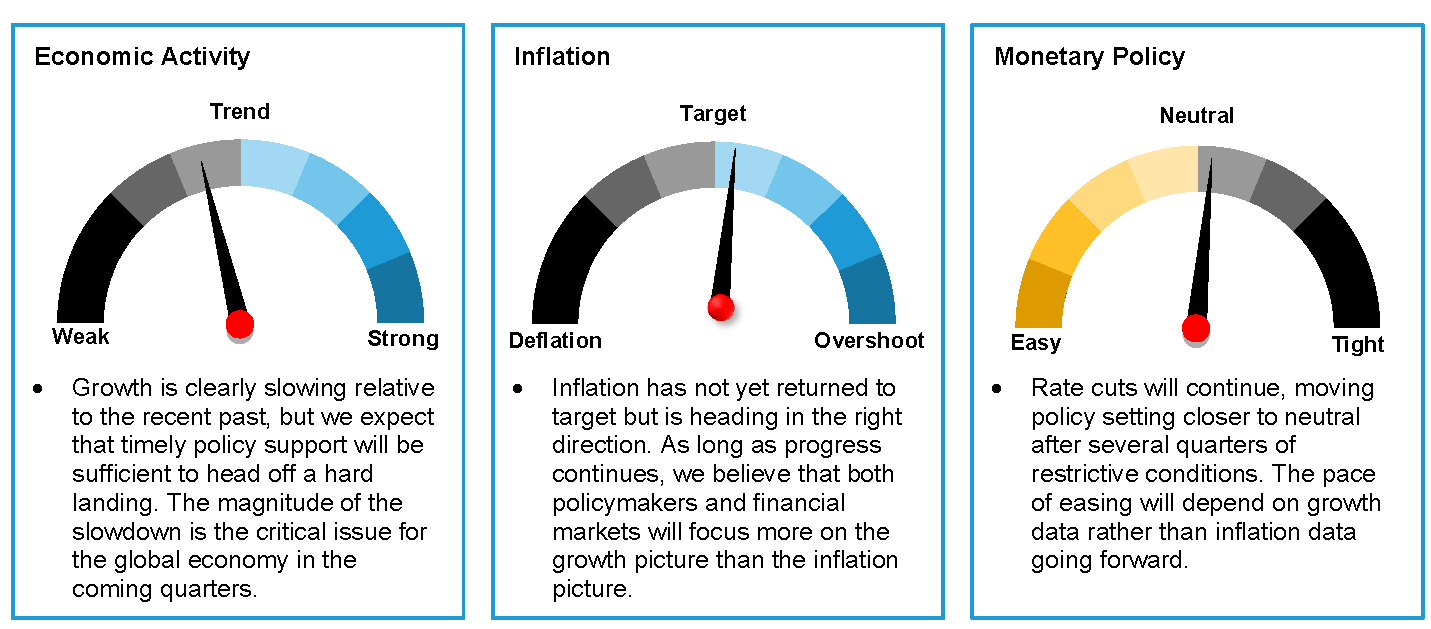

Forecast Overview