US Exceptionalism, AI and Towards the Total Portfolio

Challenges and Themes

Introduction to The Book 2026 Edition

How a New Investment Regime Could Change Investing

Implications for Portfolios and the Investment Industry

-

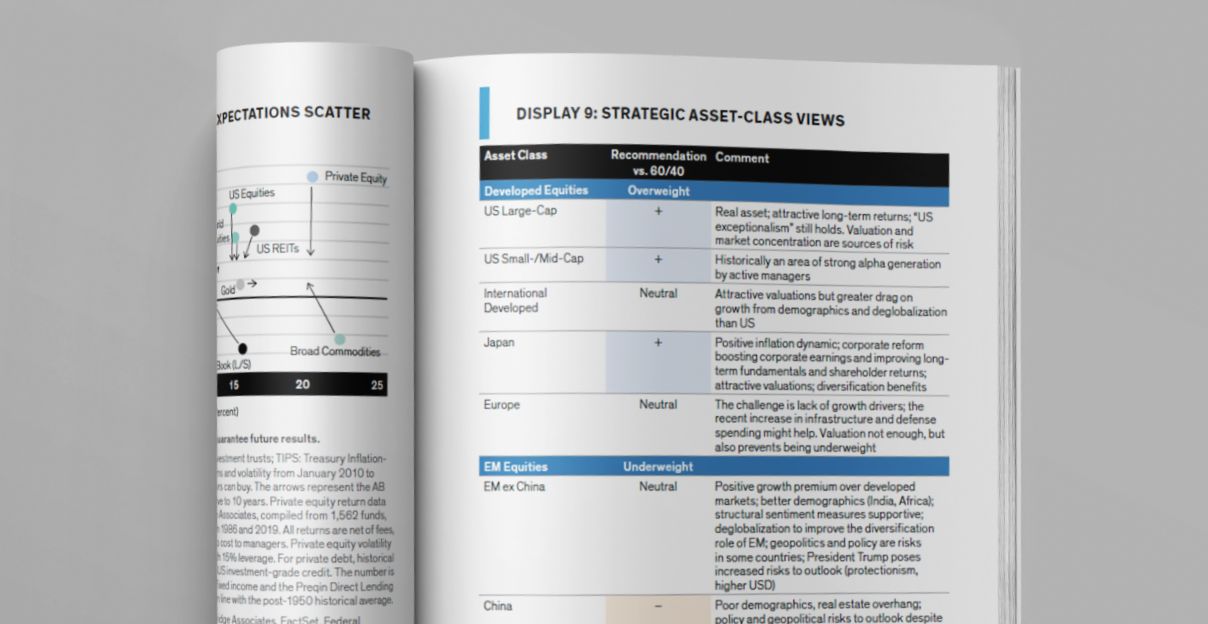

For investors who need to defend purchasing power against inflation, the outlook implies a need to have a strategic overweight in real assets—and equities are the largest real asset available.

-

We also think it makes sense to underweight nominal duration, and we continue to see value in incorporating exposure to private assets, factors and non-fiat assets.

-

Many of these positioning decisions are similar to those implied from a total portfolio approach (TPA). We see more interest in TPA, which moves beyond traditional asset-class definitions.

-

For the asset management industry, interest in multi-asset investing and OCIO mandates could increase. The industry will also play a role in tokenizing assets, facilitating allocations to illiquid real assets.

Read the Research