-

Past performance does not guarantee future results.

US Stocks

Three Reasons to Invest Now

30 August 2018

4 min read

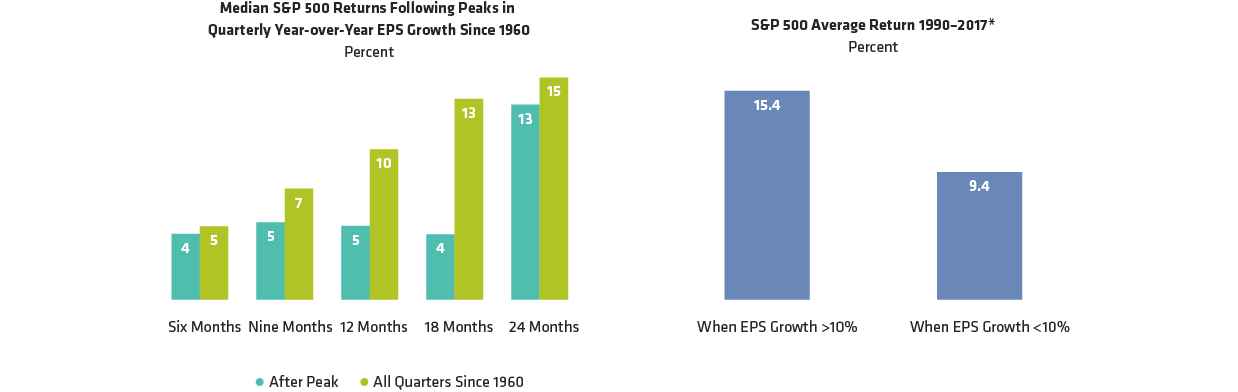

US Equities Have Delivered Positive Returns After Peaks in Earnings Growth

Left display as of July 9, 2018. Right display as of December 31, 2017

Past performance and current analysis do not guarantee future results.

*Years when earnings growth was greater than 10%: 2017, 2011, 2010, 2006, 2005, 2004, 2003, 1999, 1995, 1994, 1993. Both top-down and bottom-up EPS

Growth was >10% in all those years.

Source: Bloomberg, Bank of America Merrill Lynch, FactSet, S&P and AllianceBernstein (AB)

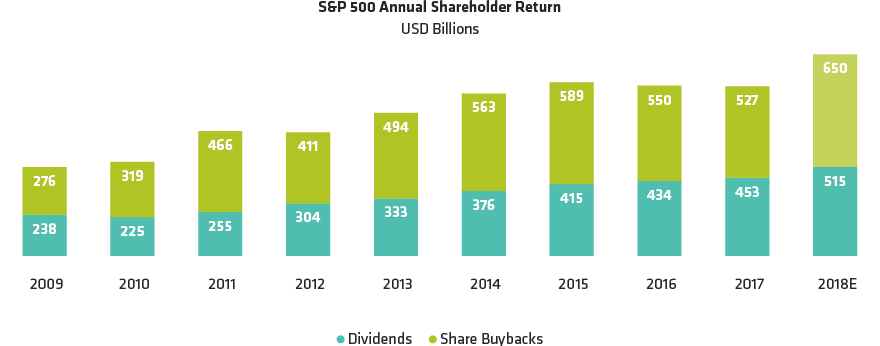

US Buybacks Poised for Further Growth

As of July 11, 2018

Current analysis and forecasts do not guarantee future results.

Source: Goldman Sachs, S&P Compustat and AllianceBernstein (AB)

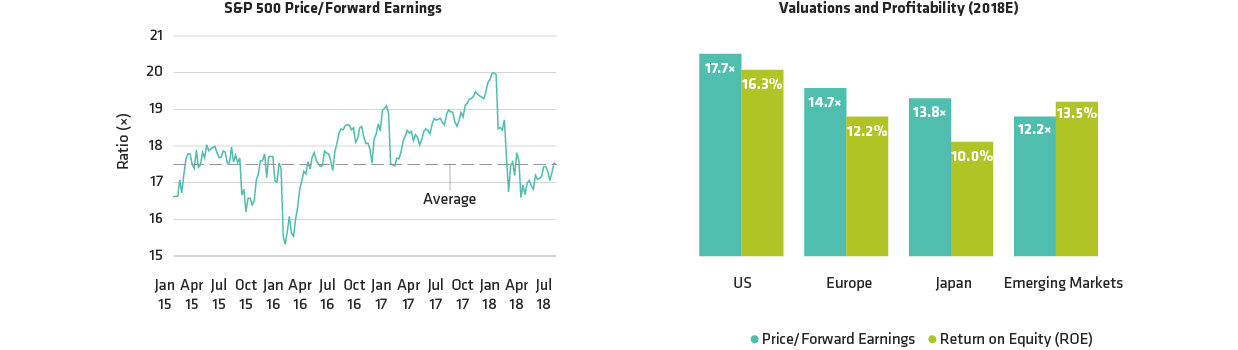

US Valuations Have Declined; Premium Reflects Higher Profitability

Data for left display through July 20, 2018; P/FE data for right display as of July 31, 2018; ROE data for right display as of July 18, 2018

Past performance and current forecasts are not indicative of future results.

Source: Bloomberg, J.P. Morgan, S&P, Thomson Reuters I/B/E/S and AllianceBernstein (AB)

-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.

About the Authors