-

Past performance, historical and current analyses, and expectations do not guarantee future results. There can be no assurance that any investment objectives will be achieved. The information contained here reflects the views of AllianceBernstein L.P. or its affiliates and sources it believes are reliable as of the date of this publication. AllianceBernstein L.P. makes no representations or warranties concerning the accuracy of any data. There is no guarantee that any projection, forecast or opinion in this material will be realized. Past performance does not guarantee future results. The views expressed here may change at any time after the date of this publication. This document is for informational purposes only and does not constitute investment advice. AllianceBernstein L.P. does not provide tax, legal or accounting advice. It does not take an investor’s personal investment objectives or financial situation into account; investors should discuss their individual circumstances with appropriate professionals before making any decisions. This information should not be construed as sales or marketing material or an offer or solicitation for the purchase or sale of any financial instrument, product or service sponsored by AB or its affiliates.

The views expressed herein do not constitute research, investment advice, or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Pushing on an Open Door

COVID-19 is Intensifying Long-term Macro Trends…Especially Debt Overhangs

September 02 2020

3 min read

137%

G-7 gross debt as percent of GDP

based on 2020 International Monetary Fund forecasts

–3%

Annualized contribution from negative real rates

to reduction in UK government debt/GDP ratio, 1946–1980

–1.3%

Required effective nominal interest rate

to keep US government debt/GDP ratio at 2021 levels

Author

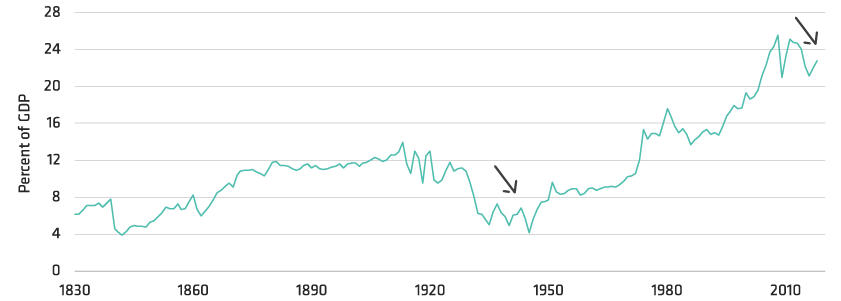

The Ebbing Tide of Globalization

World Exports as a Percentage of Gross Domestic Product

Historical analysis does not guarantee future results.

Through December 31, 2018

Source: HaverAnalytics

About the Author