-

Past performance does not guarantee future results.

European Credit

Is There Still Value in AT1s?

18 February 2020

3 min read

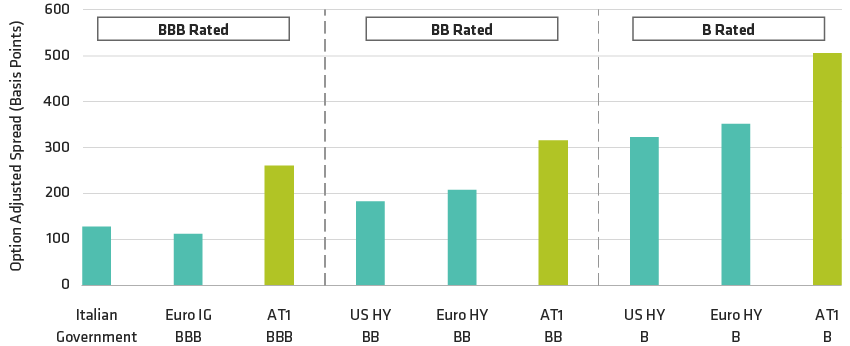

AT1 Valuations Remain Attractive

Spreads Are Still Wide Relative to Other Fixed-Income Classes

As of 31 December 2019

Analysis provided for illustrative purposes only and is subject to revision.

Source: Bloomberg Barclays and AllianceBernstein (AB)

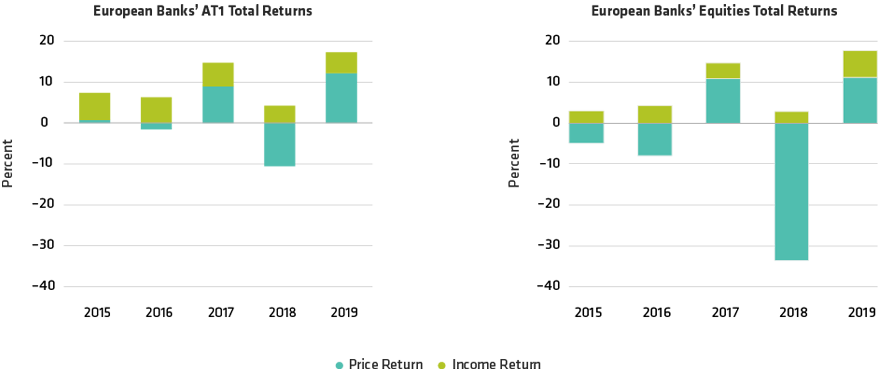

AT1s Provide Better Upside/Downside Capture

European Banks AT1 vs European Banks Equities

As of 31 December 2019

Past performance does not guarantee future results.

European Banks' equity returns based on SX7E Euro STOXX Banks Index

European Banks' AT1 returns based on Bloomberg Barclays European Banks CoCo hedged in EUR

Source: Bloomberg Barclays and AB

-

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.