The Challenge to Investors

The Impact and Broader Implications of AI

What Is The Book?

Explore the 2025 Edition

Explore Other Challenges from The Book

The future likely holds higher inflation, so investors will need to put more weight on maintaining purchasing power.

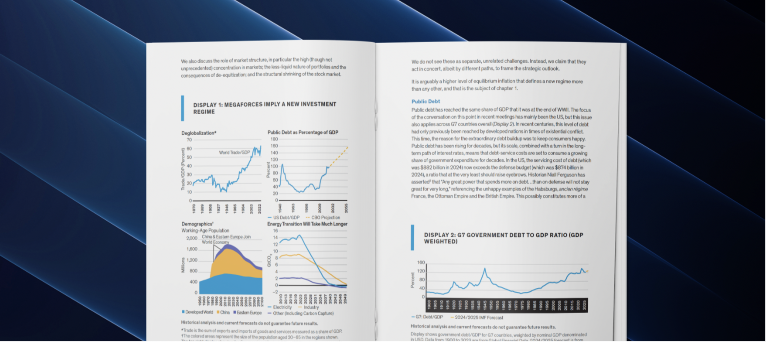

This point is highly relevant, given questions about long-term public-debt sustainability and the temptation to use inflation as a relief valve.

The government debt burden across G7 economies has returned to its lofty heights at the end of WWII, mainly to keep consumers happy.

The cost of servicing that debt is growing, and letting inflation run hotter might be the easiest political way out of the problem.

The energy transition seems to be going more slowly than initially hoped. As it stands, it may not meet the current expectations for achieving net-zero emissions by 2050. This creates additional uncertainties for investors.

Markets struggle to price the risks from geopolitics, adding another layer of uncertainty to investment plans. With geopolitical dynamics shifting, investors must take a broader view of potential future scenarios.