The Book 2025 Edition

Instability: Debt, Inflation and AI’s Impact on Investing

Challenges and Responses for Investors

Challenges and Themes for the Road Ahead

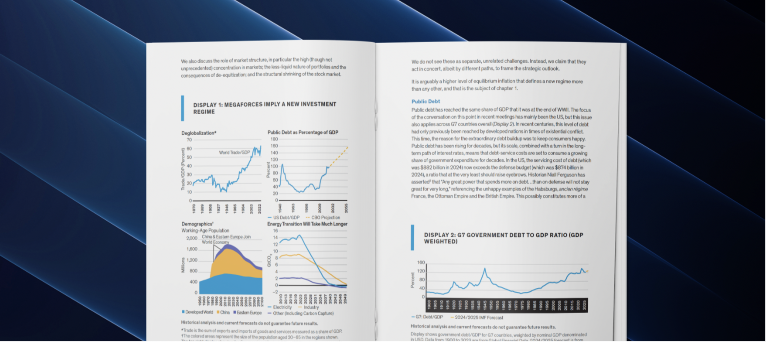

The government debt burden across G7 economies has returned to its lofty heights at the end of WWII, mainly to keep consumers happy.

The cost of servicing that debt is growing, and letting inflation run hotter might be the easiest political way out of the problem.

The future likely holds higher inflation, so investors will need to put more weight on maintaining purchasing power.

This point is highly relevant, given questions about long-term public-debt sustainability and the temptation to use inflation as a relief valve.

It’s hoped that AI will unleash a wave of productivity to counter lower economic growth. But it also brings big questions, including what the future of democracy holds and the meaning of money. These types of risks don’t tend to show up in return forecasts.

The energy transition seems to be going more slowly than initially hoped. As it stands, it may not meet the current expectations for achieving net-zero emissions by 2050. This creates additional uncertainties for investors.

Markets struggle to price the risks from geopolitics, adding another layer of uncertainty to investment plans. With geopolitical dynamics shifting, investors must take a broader view of potential future scenarios.

Responses for Investors

-

Overweight to equities, as we believe they are the largest real asset if inflation rates are elevated but not unanchored; an overweight to the US in recognition of better earnings potential

-

Significant exposure to other real assets, including inflation-protected securities, real estate and commodities. Gold and potentially cryptocurrencies may also be part of this allocation.

-

Underweight to traditional bonds, given that they could deliver lower real returns and be less effective at diversifying equity in a higher-inflation world

-

A distinct allocation to investment factors, given their potential to enhance overall portfolio returns and diversification

-

A meaningful allocation to private assets for their illiquidity premium and diversification from access to returns streams unavailable in public markets

-

Higher exposure to active strategies with potential to deliver persistent alpha—portable alpha mechanisms offer a potential solution to a mismatch of beta and alpha sources

Read the Research